The tax implications of selling a house vary depending on different circumstances such as your income level, type of capital gain, and so on. In some cases, they are minimal, while in others, they could be significant.

If you are planning to sell your house or have already done so, knowing the rules and provisions of these tax implications is crucial.

Selling your home is a big decision that can have a long-term impact. Ideally, before you put your home on the market, it’s important to know all the tax implications involved.

Your home is considered a capital asset and any net profit gained after selling the asset is assessed as capital gain hence, capital gains are subject to taxes. However, you may also get an exemption up to a specific limit under the IRS rules in certain circumstances.

Let us dive deep into the following guide about the main tax consequences of selling a home. By understanding these tax implications, you’ll be able to make an informed decision.

So, keep reading!

What Are Capital Gains Taxes?

As mentioned above in brief, capital gain taxes are the taxes imposed on capital gains. In other words, a capital gains tax is the tax that you pay on the net profit gained after selling your capital asset.

Securities, such as stocks and bonds, as well as tangible assets, such as real estate, vehicles, and boats, are subject to capital gains taxes.

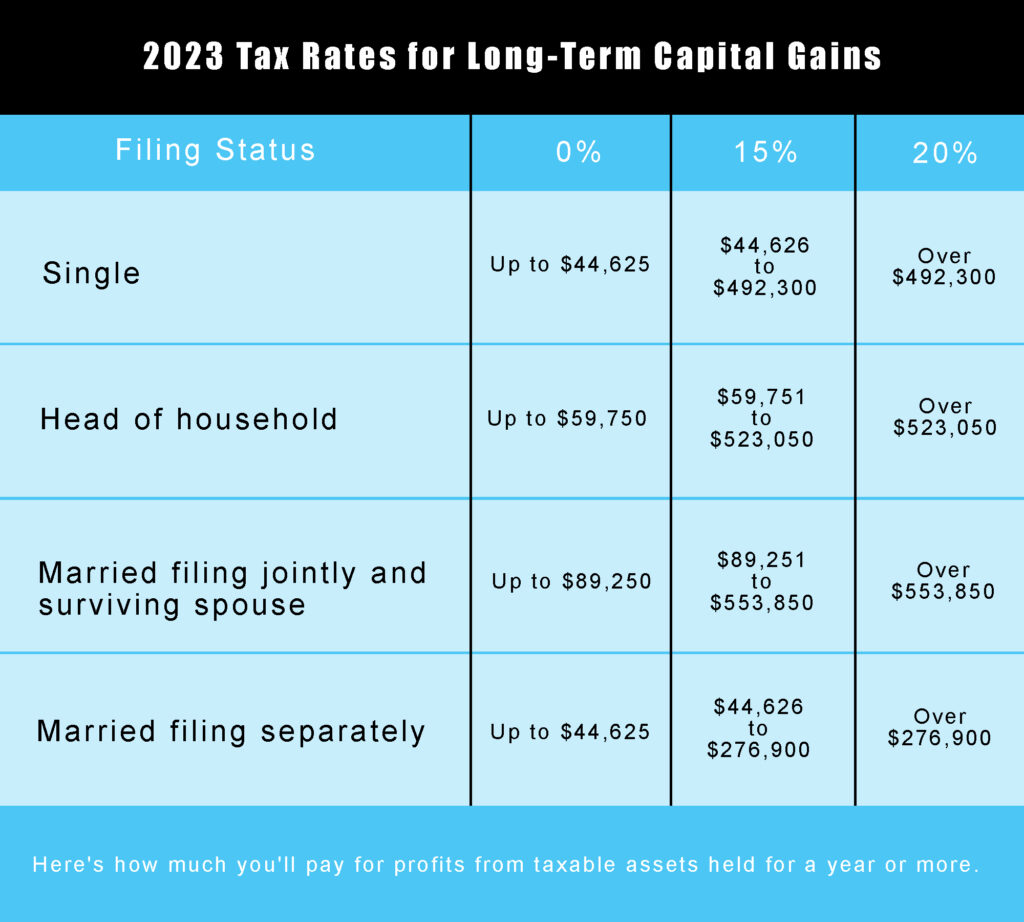

Here’s how much you’ll pay for profits from taxable assets held for a year or more.

The difference between the price you paid for an asset (your cost basis) and the price you receive when selling it (your selling price) is subject to capital gains tax by the IRS and many states.

How Does Capital Gains Tax Work?

Capital gains tax mainly depends on two main factors – your income level and how long have you owned your home. Considering these factors, you need to understand the two main categories that the IRS has divided capital gains into. These are:

1. Short-term Capital Gain – The profit that is realized from the sale of a capital asset that is held for a year or less is what we call short-term capital gain.

2. Long-Term Capital Gain – The profit that is realized from the sale of a capital asset that is held for more than a year is known as a long-term capital gain.

If you own your house for less than one year, the capital gain that you receive is consider as a short-term capital gain. Whereas, if you have owned the house for more than a year, it will be a long-term capital gain.

As a result, your tax implications will majorly depend on these circumstances and your income.

How Much Is The Tax?

You will be subject to taxation at your standard tax rate if you have a short-term gain. With preferential tax treatment, long-term capital gains are on tax at a rate of 0%, 15%, 20%, or 28%.

However, your income and tax filing status affect these rates.

According to IRS.gov, if your taxable income is less than or equal to $40,400 for single filers, $80,800 for married couples filing jointly, or qualifying widow(er), then some or all of your net capital gains may be subject to 0% tax.

How To Avoid Capital Gains Tax On The Sale Of Your House?

Homeowners are also eligible for a write-off from the IRS, which allows single filers to exclude up to $250,000 of profits and married couples filing jointly to deduct up to $500,000.

You are require to pay capital gains tax on the excess gain if you sell your house for a net profit exceeding $500,000 (for couples filing jointly) or $250,000 (for singles).

For instance, capital gain would be $800,000 if you and your spouse purchased your home for a cost basis of $200,000 and sold it for $1,000,000 many years later.

If you qualify for the specified exclusion, then $500,000 of this would be tax-free, but the remaining $300,000 would be a taxable capital gain.

To qualify:

- You must have owned the property for at least two of the previous five years.

- You must have lived in it as your primary residence for at least two of those five years to be eligible. The ownership and residence requirements do not have to be met simultaneously in the same two years.

- Additionally, you cannot have used the exclusion on a different house within the two years before the sale.

When Is The Capital Gains Tax Due?

You need not need to pay the capital gains tax until you sell your property. You owe any capital gains taxes for the sale of your house at the tax deadline associated with the year the sale closes.

The IRS recommends following their guidelines on this matter because there are several situations that may require you to make estimated tax payments.

Want to avoid writing a sizable check at tax time? Hence, it could be a good idea to report your estimated capital gains tax to the IRS as soon as the sales transaction closes.

The Final Say

When you sell your house, it’s important to be aware of all the tax implications of selling a house. The amount of tax you pay depends on various factors such as the value of the property, your income level, the period for which you are holding your property, and so on.

To reduce your tax burden, do your research to lay out all of your tax options and make sure that you are fully aware of your obligations.

As a last note, it’s important to emphasize that capital gains taxes can be a tricky subject with a lot of grey areas. It’s crucial to seek advice from an expert, licensed tax professional, specifically one who specializes in real estate matters. For more questions on Tax Implications Of Selling A House you can contact us.

Looking for more profound guidance? Get in touch today with Elite Properties!