We Buy Homes for Cash: A Straightforward Path When You Need Certainty

New York real estate is famous for moving fast until it doesn’t. A listing can sit. A buyer can disappear. A “great offer” can turn into weeks of inspections, renegotiations, and lender delays.

That’s why more owners look for a direct buyer when life gets complicated. For owners who want a direct sale, Elite Properties NY can act as a direct buyer rather than taking the traditional listing route. We make offers, purchase properties directly, and close on timelines that make sense for real people.

If you are looking for companies that buy houses for cash, your search is about more than just finding a buyer. You are essentially trying to solve a puzzle. You need a straightforward decision and a concrete path forward. Most of all, you want an exit strategy that does not involve turning your daily life into a full-time real estate project.

From the seller’s side, the hardest part is usually the uncertainty. You can do everything “right” and still end up stuck: waiting on a lender, dealing with inspection demands, juggling showings, or losing time while someone decides if they “still love it.”

That uncertainty is expensive in New York. Mortgage payments, taxes, insurance, and utilities don’t pause just because the sale is taking longer than expected. According to recent market data and trends, extended holding periods and the risk of a deal falling through can significantly eat away at a seller’s final bottom line.

From the seller’s side, there’s also the reality that not every home fits the traditional retail lane. Some properties are dated. Some are inherited and still full of belongings. Some have tenants, violations, or deferred maintenance that makes a standard listing feel like a battle.

And in the toughest cases, owners need to sell fire damaged house properties where repairs, remediation, and insurance conversations stack up quickly. When that happens, many sellers aren’t looking for a “perfect strategy.” They want a practical exit and a timeline they can plan around.

Now here’s how we look at it. From Elite Properties NY’s side, our role is simple: assess the property as it sits today and decide what we can pay based on real-world cost and risk.

When we say we buy houses in any condition, we mean we don’t require you to repaint, renovate, stage, or “make it market ready” to start the conversation. Condition matters to price, but it doesn’t block the process. We evaluate:

- Location and neighborhood trends.

- Property type (Single family, multi-family, etc.).

- Occupancy status and potential legal hurdles.

- Repair scope required for the next chapter.

From Elite Properties NY’s side, the goal is clarity, not drama. A direct sale works best when the expectations are clean: we buy homes as-is, we’re taking on the post-closing work, and you’re getting a straightforward offer you can accept or decline without pressure. This is why people choose companies that buy houses for cash, not because they don’t care about value, but because they care about certainty.

What the process looks like (without the fluff)

When we buy homes for cash, we start by learning what you’re working with and what timing you need. Some owners send a few photos and notes; others prefer we take a quick look in person so we can be accurate.

Then we share a written offer that matches the home’s current state and the work we’re taking on. Take a look, and if it works for you, we proceed; if it doesn’t, you can simply decline.

If you accept, we move into title and closing coordination. In many cases, cash deals move faster simply because there is no lender underwriting, no lender-required appraisal, and no financing contingency to manage. That’s one of the biggest reasons sellers search cash for houses in the first place.

What can change the offer

Sellers often ask, “What do you look at?” The biggest factors are straightforward: location, overall condition, property type, occupancy, and title complexity.

- If the home needs major work, the offer reflects that work.

- If there are tenants, we factor in the added coordination.

- If you’re trying to sell fire damaged house property, we look at the scope: smoke, structural impact, electrical, and water-related issues from firefighting.

Again: it’s not a judgment. It’s the math of what it takes to take responsibility for the property after closing.

Final Thoughts on Selling Your New York Home for Cash

A traditional sale can work well when a home is turnkey and time is on your side. But when you want speed, simplicity, and fewer moving parts, a direct buyer can be the better fit.

Elite Properties NY exists for that lane. We buy homes for cash, we evaluate properties honestly, and we keep the process clear so you can make a decision and move forward, especially when the usual listing route feels like too many unknowns.

FAQs

1) Are you one of the companies that buy houses for cash in New York?

A: Yes. Elite Properties NY buys properties directly, and we can close with cash, so the deal isn’t dependent on a buyer’s mortgage approval.

2) Do you really buy houses in any condition in New York?

A: Short answer: Yes. Long answer, we buy houses in any condition, from the ones that are move-in ready to those that need serious repair. The thing worth noting is that Condition affects price and not eligibility

3) Can you help if I need to sell fire damaged house property?

A: Often, yes. We review fire-related damage case by case and can make an as-is offer when it’s a fit.

4) Is cash for houses always “faster”?

A: It’s usually faster because there’s no bank underwriting or appraisal timeline, but closing speed still depends on title and paperwork.

5) Will I have to clean out the home first?

A: In many cases, sellers choose a direct sale specifically to avoid a long cleanup and prep cycle. Tell us what you’re dealing with and we’ll explain what is realistic for your situation.

A house fire changes your day in seconds. After the trucks leave and the smoke clears, you’re often staring at the same questions most homeowners never plan for: Is the place safe? Can I even stay here? Do I repair it, or do I just sell and move on?

If you’re reading this because you need to sell your house after a fire, take a breath. You do have options in New York. The best route depends on how serious the damage is, how quickly you need to act, and whether you want to repair the property or sell house as-is.

Step 1: Understand What “Fire-Damaged” Means in Real Life

Fire damage isn’t one single category. Two homes can both be called “fire-damaged” and look completely different. After a fire, you can usually see the surface issues quickly, but the “real story” takes a closer look. It is what lies beneath that requires special attention, wiring, framing, or any damp areas that need time to dry, whereas smoke marks and residue are easier to spot.

To get moving without guessing, focus on two basics:

• A quick walk-through from a contractor to highlight the real problem areas

• Your insurance position, at least at a high level (what’s covered, what’s delayed, and what’s still being decided). You don’t need every answer on day one. But you do need enough facts to avoid spending money in panic or getting stuck in limbo.

Your Options for Selling a Fire-Damaged House in New York

Option 1: Repair, then list on the open market

This route is often best when the damage is limited, and you’re in a position to fund and manage the repairs. Once the home is restored, you may get a broader buyer pool and a stronger price. That being said, getting this done is a different beast altogether; there is a whole host of variables to be considered: NY permits, inspections, contractor availability, and the surprises that pop up once the work begins. Fire repairs may also require additional permits, documentation, especially when structural, electrical, or remediation work is involved.

If your goal is to sell quickly, this route can start to feel like progress comes in stops and starts.

Option 2: Sell as-is to an investor or cash buyer

If your main goal is speed, simplicity, or avoiding a long rebuild, you can sell fire damaged house in its current condition. This is where companies that buy houses often come in, especially buyers offering cash for home who are prepared for rehab work.

A direct as-is sale typically appeals to sellers who don’t want to manage cleanup, contractors, or weeks of back-and-forth. You’re basically trading “top market price after renovation” for a cleaner process and fewer delays.

If you want to sell house as-is and avoid turning this into a months-long project, this is often the most straightforward path.

Option 3: Do a small cleanup, then sell as-is

Some sellers take a middle route: clear debris, address basic safety, and make the home easy to access, then sell house as-is. This isn’t a renovation. It’s more like “making the property presentable enough for a serious evaluation.”

This can help a buyer assess the home faster and sometimes reduce confusion around the scope of damage.

Timing Overview: What to Expect

The Truth is: Timelines vary. In New York, timing usually breaks into a few common tracks:

• Repair and list: can stretch across months, influenced by permits, inspections, and contractor timing

• As-is sale to a cash buyer: can close sooner, since you’re not waiting on repairs or lender sign-off

• Light cleanup + as-is sale: depends on how quickly you can clear access and address the basics

If you’re paying holding costs, mortgage, taxes, utilities, or the home is sitting empty, every extra week adds up. Setting a realistic timeline early helps you pick the option that matches your situation, not just the “ideal” plan.

What Buyers Often Ask After a Fire

Whether you list traditionally or go as-is, expect questions like:

• Is the cause of the fire known?

• What was affected, smoke, structure, electrical, or water-related damage?

• Are utilities on, or were they turned off afterward?

• Has any cleanup happened yet (soot, odor, drying, mold prevention)?

• Where does the insurance claim stand right now, open, pending, or closed?

You don’t need a perfect folder of documents on day one. Just be consistent about what you know, and upfront about what you’re still confirming, it prevents confusion later.

How Elite Properties NY Can Help

If you’re dealing with fire damage and want a simpler route, Elite Properties NY can review the property and explain what a direct sell house as-is option would look like. If it makes sense for the property, they can share a clear offer. This option is often chosen when the goal is fewer steps and a simpler closing.

Conclusion:

After a fire, decisions tend to come quickly. Start with the facts, then choose the route that fits your timeline, repair and list, sell house as-is, or do a small cleanup and sell.

If speed is the priority, working with companies that buy houses and offer cash for home can be a practical option, especially when you want to sell fire damaged house without taking on a long rebuild.

FAQs:

- Can I sell a fire-damaged house in New York without repairing it?

Yes. Plenty of owners sell house as-is, especially when repair costs are high or the rebuild timeline doesn’t fit their situation.

- Does selling as-is usually affect the price?

Usually, yes. The offer often reflects the repair cost and risk the buyer is taking on.

- Do cash buyers really buy home as-is after a fire?

In many cases, yes. The buyer will look at things like where the home is, how the damage affects the main systems, and whether the property can be evaluated safely.

Foreclosure in New York

Foreclosure is a word most people only look up once it’s already on their mind. In New York, lenders usually kick it off by filing a foreclosure lawsuit after payments have been overdue for a while. It’s not one-and-done; once court mail and formal notices arrive, the window to act can feel smaller.

If you’re trying to Avoid foreclosure in New York, it helps to pin down your current stage, read what the latest notices are telling you, and decide what to do next while you still have options.

Foreclosure, Without the Legal Jargon

A mortgage is a loan tied to your home, and the home secures that loan. After a payment is missed, most lenders begin with late notices and follow-ups to collect. If the loan remains unpaid, they may move forward and ask the court to enforce the loan terms.

New York typically uses a court-based foreclosure process. You’ll likely get notices, mailings, and deadlines you can’t ignore. The fine details vary, but the order of events is often similar.

How the Foreclosure Process Commonly Unfolds

1) Missed payments and notices

It usually begins with a missed payment, then another, and the costs and notices start to build. Most people think they’ll fix it quickly, but the longer it drags on, the harder it can be to get back to “current” status.

2) The lender files a case

If the balance still isn’t brought current, the lender may file in court. That’s usually when it turns formal: legal papers arrive, response dates start counting, and the case moves forward on a court schedule.

3) Settlement talks or loss-mitigation options

In many situations, you can still look at alternatives, like a modification, a repayment plan, or other lender options intended to cure the default and keep the case from advancing.

4) Judgment and auction (or transfer)

If nothing is agreed to, the case may continue toward judgment and a foreclosure sale/auction. As that happens, timing becomes tighter and the number of workable options usually drops.

Options That May Help You Avoid Foreclosure

Every homeowner’s situation is different, but these are common paths people explore:

1) Bring the loan current

If you can catch up (sometimes with help from family, refinancing, or a structured plan), that can stop the process. The challenge is timing, many people try this after the numbers already feel unmanageable.

2) Loan modification or repayment plan

Some lenders will consider adjusting terms. It’s paperwork-heavy, and results vary, but it can be worth exploring early.

3) Short sale

A short sale means selling the home for less than what is owed, with the lender’s approval. This is not always simple, and many sellers prefer to work with Short sale specialists NY because the lender approval process and documentation can be intense.

4) Sell the home before foreclosure finishes

For many people, selling is the cleanest way out, especially when the monthly payment no longer fits the budget. If your priority is speed, you may be thinking: “How do I Sell my house fast without repairs, showings, and delays?”

That’s where companies that buy houses for cash can be an option. A direct cash sale won’t fix every situation, but it can help some homeowners avoid the uncertainty of waiting for an auction date.

Selling “As-Is” When the Home Isn’t Perfect

Foreclosure risk often shows up alongside home-condition problems, repairs you’ve postponed, tenant situations, or damage that makes listing harder. Traditional buyers may expect inspections, lender conditions, and repair negotiations that slow the timeline even more.

If you’re dealing with major damage, you might be looking for a way to sell fire damaged house without taking on a renovation project.

This is where sellers look for buyers who say things like we buy houses in any condition and we buy houses as is, because the home selling process is more direct, and you’re not expected to fix everything first.

At Elite Properties NY, we purchase homes in New York in a straightforward way, including properties that are outdated, distressed, or difficult to list. If you’re facing foreclosure timelines, a direct sale can be a practical alternative to dragging through months of uncertainty.

Conclusion

Foreclosure moves in stages, and each stage can narrow your choices. First, confirm your stage. From there, pick the option that matches your reality: catch up, negotiate with the lender, try a short sale, or sell before the case gets close to a sale date. If you’re short on time, an as-is buyer may help you move faster and reduce the pressure.

FAQs

1) How long does foreclosure take in New York?

There isn’t a single “normal” timeframe. How quickly it moves varies by lender and by county, plus how fast documents and replies are handled. If notices are showing up, don’t ignore them, consider speaking with a housing counselor or an attorney.

2) Can I sell my home if foreclosure has already started?

In many situations, yes, especially if you begin while there’s still time to close. Getting started sooner usually makes everything less rushed.

3) Short sale vs. foreclosure: what’s the difference?

In a short sale, the lender agrees to a sale price that won’t fully cover the remaining mortgage balance. Foreclosure is different: it’s the lender’s legal route to take the property back after a default.

4) Do cash buyers really purchase homes in poor condition?

Some do. Many sellers choose this route specifically because we buy houses in any condition and we buy houses as is options avoid the repair and listing cycle.

5) Will selling fast stop foreclosure automatically?

Not automatically. It depends on timing and closing. If you’re close to key deadlines, move quickly and get professional guidance to coordinate the sale.

Introduction

Selling your first home in NYC? Man, it can feel like you’ve signed up for a reality show! The 2025 market’s buzzing, new contracts jumped 5.8% since last year, and the median price is hovering around $1.1 million as of May. Whether you’re in a swanky Manhattan pad or a charming Queens rowhouse, it’s a tough crowd out there. Inventory’s up 11.2% year-over-year, so buyers are spoiled for choice. At Elite Properties, we’ve guided plenty of first timers through this chaos, often with quick cash deals. Grab a bagel, and let’s walk through some real talk on selling your NYC home in 2025.

Getting a Feel for the 2025 Scene

First off, let’s get a grip on what’s happening. NYC’s real estate is a moving target, prices swing from $1.495 million in Manhattan to $695,000 in Queens. Mortgage rates are settling around 6.67%, nudging some buyers toward cash to skip the loan hassle. I heard from a friend in the Bronx that homes move faster when priced right, especially with that 6% price bump there. We at Elite Properties love breaking this down for you, so you’re not guessing what’s hot and what’s not.

Making Your Home Shine

Tip 1: Take a Good Look Around

Walk through your place like it’s your first day moving in. Notice that leaky faucet in the kitchen or the scuff on the living room wall? In NYC, where space is gold, fixing these little things can win over buyers, especially cash ones who want no fuss. I once helped a seller in Brooklyn repaint a dingy hallway, and it bumped their offer by a few grand. We can steer you to the fixes that count.

Tip 2: Ditch the Clutter

NYC homes can feel tiny, so clear out the personal stuff, those family pics, that funky lamp you love. Let buyers imagine their own life there. A friend staged her Astoria apartment by boxing up half her books, and it felt twice as big. Less clutter, more appeal—that’s the trick.

Tip 3: Maybe Try Staging

Staging’s not just for fancy lofts. A pro can make your place pop, whether it’s a cozy Bronx studio or a Staten Island house. I saw a staged home in Queens snag a higher offer because it looked move-in ready. Elite Properties can hook you up with someone who knows the local vibe without costing a fortune.

Nailing the Price

Tip 4: Peek at What’s Selling Nearby

Don’t just throw out a number, check what similar homes in your area went for. Queens prices shot up 10.6% this year, and the Bronx isn’t far behind at 6%. We dig into these details at Elite Properties to give you a cash offer that feels fair and fits the market.

Tip 5: Don’t Shoot for the Moon

Overpricing can leave your home sitting there like a stale bagel. With more listings out there, a realistic price pulls in buyers fast. I’ve seen folks in Brooklyn learn this the hard way—price too high, and you’re waiting months. We’ll help you find a number that works.

Picking Your Selling Style

Tip 6: Go Cash if You Can

Cash for home sales? They’re a lifesaver here. No bank delays, no back-and-forth—just a quick deal. In NYC’s rush, cash buyers love the speed. Elite Properties makes it smooth with offers that close in days, perfect if you’re eager to move on.

Tip 7: Cash or Traditional—What Feels Right?

Traditional sales mean realtors, open houses, and those chunky 5-6% closing costs NYC loves. Cash sales skip all that mess. A neighbor went cash with us and closed in a week—no stress. It’s your call, but cash can be a breeze with Elite Properties.

Tackling the Details

Tip 8: Sort Out the Paperwork

NYC’s got its quirks—disclosures, transfer taxes, maybe a co-op board nod. It can feel like a puzzle for a first-timer. We handle that stuff at Elite Properties, so you’re not drowning in forms.

Tip 9: Stick with People You Trust

The cash-for-home game can have some shady characters. Go with a crew that knows NYC inside out. Elite Properties has been around, selling millions in real estate, and we keep it straight with you every step.

Showing Off Your Spot

Tip 10: Get Online and Stand Out

Buyers here live online, great photos and a solid write-up are key. Our website puts your home in front of cash buyers scrolling through listings. We make sure it catches their eye in this fast city.

Tip 11: Shout About What’s Cool

Got a subway stop nearby or a view that kills? Maybe your place has green upgrades thanks to Local Law 97? Play those up! A friend sold her place faster by mentioning the rooftop deck. Elite Properties helps you highlight what makes your home a gem for cash buyers.

Wrapping It Up

Selling your first NYC home in 2025 doesn’t have to be a marathon. Tidy it up, price it smart, pick a selling style, and lean on folks who get it. Elite Properties is here with fair cash offers and a team that’s got your back. Ready to dive in? Check out our official website for an offer, and let’s get your home sold in this crazy market!

Introduction

Selling your house is a big deal, it’s not just about the money, but all the memories tied to it. If you’re in New York thinking, “Should I sell now?” You’re not alone. The market here is a wild ride, shaped by the economy, buyers, and your own life. At Elite Properties NY, we’re here to help. We’ll share some insights on when to sell, guide you through the process, prove why cash buyers like us keep it fast and smooth, and handle any questions you throw our way.

What is the current state of New York’s housing market?

Right now, everything from mortgage rates to neighborhood demand, and the bigger economic picture, is mixing things up. In Brooklyn and Queens, plenty of buyers are still hunting, while other neighborhoods are a bit quieter, partly because of the season or local money concerns.

Before selling, think about:

- Neighborhood Vibe: If houses nearby are selling quickly, you could get a higher price. But if the market feels a little sluggish, exploring cash offers might be smart.

- Your Situation: You might be dealing with foreclosure worries, relocating, downsizing, or owning an inherited place you don’t really want.

- Home Condition: If repairs are on your mind, selling as-is to a cash buyer can spare you the expense and hassle.

From Manhattan to Long Island to Upstate, Elite Properties NY tailor a plan for you.

The Traditional Home Selling Process

Selling the old-school way can feel like a second job, especially if your home needs work. Here’s the deal:

- Fix It Up: Clean, declutter, stage, and maybe shell out for repairs to wow buyers. This can drag on for weeks.

- Get a Realtor: They list your place, drum up interest, and line up showings. In New York,1–3% expect 5% to 6% in commissions.

- Open Houses: Having strangers walk through at all hours can disrupt your daily routine and keep you tidying up endlessly.

- Negotiate Offers: Deals can fall apart over inspection results or financing hiccups, sometimes stalling things or stopping them altogether.

- Closing: The closing phase can run anywhere from a month to three months, and you’ll usually pay another 2–3% in closing costs.

For many New Yorkers, this is a headache, especially if time or cash is tight. That’s where cash buyers like Elite Properties NY come in handy.

Why Choose a Cash for Home Buyer?

If you’re thinking, “I really need to sell my house quickly,” a cash buyer can be the answer. At Elite Properties NY, we buy houses directly, as-is, across NYC, Long Island, and beyond, all for cash.

We can close in a week, not the 60-day traditional sales average in New York. No showings, no open houses, no back-and-forth. We take homes in any shape, worn out, empty, with tenants, or facing foreclosure. Got junk you don’t want? Leave it, we’ll deal with it.

We cover all closing and legal costs, so no fees or commissions. In a rush? We can close in days. Need time? We’ll pick a date that fits, even months out. Cash offers usually land at 60-85% of market value due to speed, but we strive for fairness based on your home and area. We’ve been a trusted name since 2009.

When Should You Sell?

Still on the fence? The answer often ties back to what’s happening in your life right now.

- Money Troubles: If you’re behind on payments or foreclosure feels close, a quick cash sale could help clear what’s owed so you can move on.

- Moving or Downsizing: Got a new opportunity or thinking of scaling down? We can keep it simple and work around your schedule.

- Inherited Homes: If you’ve come into a property you don’t need, we’ll buy it exactly as it is, no fixing or cleaning required.

- Fixer-Uppers: Old roof, outdated kitchen, or other headaches? Sell as-is and skip the renovation costs.

If your home’s in good shape and you’ve got time, a realtor or FSBO might get you more, but it takes patience and upfront effort.

How Elite Properties NY Works

Since 2009, we’ve kept selling simple. Here’s how:

- Contact Us: Call 917-722-1272 or fill out our website form with your details.

- Home Visit: We’ll check your place and give a no-pressure cash offer in 24–48 hours.

- Accept the Offer: Like it? We handle paperwork, and you’ve got three days to back out.

- Close Your Way: Pick a date, next week or months out. We manage it all, and you get cash.

Other Selling Options

Cash deals are quick, but they’re not the only game in town. You could also look into:

- Realtor: If your property is move-in ready, an agent may help you get top dollar, but expect to pay commissions and wait longer.

- FSBO: Selling on your own cuts out the agent’s fee, though you’ll handle marketing, showings, and negotiations. A flat-fee MLS can help get your listing noticed.

Choosing a Trustworthy Cash Buyer

Not all cash buyers are the same, so check carefully:

- Check Reviews: Past client feedback tells you a lot.

- Avoid Lowballs: If you see offers far under 50–70% of value, think twice and shop around.

- Ask Questions: We’re happy to talk through every step so you know what to expect.

FAQ – What People Often Ask

- Any fees or commissions?

No. We cover all legal and closing costs, so what we offer is what you take home.

- Can I sell if I’m in foreclosure?

Definitely. A fast cash sale can help pay off debt and move forward.

- What properties do you buy?

Pretty much any residential property, houses, condos, multi-family buildings, empty or tenant-occupied, across New York.

- Is Elite Properties NY trustworthy?

Absolutely. We keep every step transparent, explain your options up front, and put everything in writing so you know exactly what to expect.

Conclusion

Selling in New York’s fast 2025 market depends on your situation, timing, and property condition. If you’re looking for a quick, stress-free sale without repairs or hidden costs, Elite Properties NY is ready to help. Since 2009, we’ve offered fair cash deals and flexible closings to fit your timeline. Thinking about making a move? Call 917-722-1272 or check out our website for a free, no-obligation cash offer. We’ll handle the details so you can look ahead.

Disclaimer: This article shares general information only. For financial, tax, or legal guidance tailored to your situation, it’s always smart to speak with a qualified professional.

Introduction

Homeowners facing financial difficulties often find themselves at a critical crossroads: Foreclosure vs Short Sale, which is the better option? The critical nature of mortgage debt demands homeowners need to grasp the consequences of both foreclosure and short sale before making a final decision.

When homeowners must exit the mortgage market through foreclosure or short sale, they encounter completely different financial as well as credit and emotional outcomes. Further in this blog, it explains how to compare different choices along with their effects, as well as presents evidence that showing your home to someone who pays cash makes the most financial sense. The blog presents strategic approaches combined with methods to handle these situations while strengthening financial security for the future.

Understanding Foreclosure: How It Works & Its Consequences

A homeowner’s inability to make mortgage payments allows lenders to start legal foreclosure proceedings that end with the sale of the property. The home selling process in foreclosure typically follows these steps:

- Missed Payments: Repeated payment default triggers the lender to send out a Notice of Default (NOD).

- Pre-Foreclosure Period: Homeowners during the pre-foreclosure period have the potential to pay off their debt while attempting negotiations with lenders to perform short sales.

- Auction Sale: Property sale through auction happens when all attempts to find solutions fail and the property is sold at prices lower than market value.

- Eviction & Credit Damage: After auction failure, the lender becomes property owner, which results in homeowner eviction while their credit score suffers damage.

Consequences of Foreclosure:

- Severe credit damage: The process of foreclosure damages credit score severely by 100 to 160 points and stays visible on reporting systems for seven years.

- Legal implications: The law allows lenders to obtain remaining debt known as deficiency balance after foreclosing on a property.

- Loss of control: When the homeowner has to go through foreclosure, the lender stands as the leader in all decisions, thus restricting the homeowner from making choices about the property’s end sale.

- Difficulty in future home purchases: Multiple mortgage providers tend to avoid granting loans to people with recorded foreclosure activities.

The Short Sale Process for Homeowners: A Viable Alternative?

Short sale is where the homeowner sells the property below the outstanding mortgage value, but with the lender’s permission. The Homeowner’s Short Sale Process is the following:

- Contacting the Lender: The homeowner must prove financial hardship and request short sale authorization.

- Listing the Property: The property is put on sale, typically at market value, with the lender’s consent.

- Negotiation & Offer Approval: Upon receiving an offer, the lender must approve the price and terms of sale.

- Closing the Deal: If approved, the property is sold, and the lender forgives the balance or negotiates a payment schedule.

Advantages of a Short Sale:

- Less impact on credit: Credit scores will typically drop by 50-120 points, and the short sale is on the credit report for four years or less.

- Faster financial recovery: Homeowners can qualify for a new mortgage sooner than they would after a foreclosure.

- More control over the sale: The homeowner actively finds a buyer and negotiates terms.

- Potential debt forgiveness: Most lenders forgive the unpaid balance of the mortgage.

Foreclosure vs. Short Sale: Head-to-Head Comparison

| Factor | Foreclosure | Short Sale |

| Credit Score Impact | Severe (100-160 points lost) | Less severe (50-120 points lost) |

| Time on Credit Report | 7 years | 4 years or less |

| Ability to Buy Again | 5-7 years | 2-4 years |

| Process Complexity | Automatic lender repossession | Requires lender approval |

| Financial Relief | No negotiation, full debt may still be owed | Possible debt forgiveness |

| Control Over Sale | None (lender controls it) | Homeowner negotiates sale |

| Emotional Impact | Stressful, damaging to reputation | Less stigma, more control |

Selling a Home in Foreclosure: Is a Cash Buyer the Best Escape?

If facing foreclosure, selling to a cash buyer can be a smart, fast alternative to either foreclosure or a short sale. Here’s why:

- Quick closing: Cash buyers can finalize the sale in days, preventing foreclosure.

- No lender approval required: Unlike a short sale, cash sales bypass the need for lender approval.

- No repairs or realtor fees: Cash buyers buy houses in as-is condition, making it cheaper and quicker for homeowners.

- Less stress and uncertainty: Homeowners eliminate lengthy negotiations and foreclosure proceeding risk.

- Elite Properties deals in homes in as-is condition, which makes the transaction quick and easy.

Which Is the Better Option for You? A Decision Framework

Short Sale is the Better Option If:

- You prefer to avoid credit damage.

- You can still negotiate with your lender.

- You desire an opportunity to purchase a home again earlier.

- You are willing to undergo the lender-approval process.

Foreclosure is the Only Option If:

- You have depleted all Avoid Foreclosure Options (loan modifications, refinancing, etc.).

- You are unable to sell it or negotiate a short sale in time.

- You are unwilling or unable to pursue the home selling process further.

Selling to a Cash Buyer is the Smartest Move If:

- You need to sell a foreclosure home fast with less stress.

- You don’t want to deal with lender negotiations.

- You want a quick, easy transaction with cash payment assurance.

- Elite Properties provides a hassle-free cash-buying experience, allowing homeowners to avoid foreclosure through an instant sale.

Conclusion: Making an Informed Decision

It is not an easy decision to choose between foreclosure and a short sale, but having the final impacts of each in mind can help the homeowner feel secure in a decision. In most cases, a short sale is a preferable situation for homeowners who want to avoid further hurting their credit while regaining financial health sooner. Yet, under the circumstances that time and solutions are short in supply, foreclosure may be the only way.

With no repairs to perform, no holdups in lender approval, and a quick closing process, Elite Properties provides an easy way to sell an ugly property. Taking proactive measures, seeking professionals, and examining all the possibilities can become the turning point in having a secure future financially.

Ultimately, it will depend on your financial situation and future needs. The important thing is to act early, shop around, and select the option that reduces harm and maximizes recovery and future home ownership opportunities.

Frequently Asked Questions (FAQs)

- What is the primary distinction between a short sale and a foreclosure?

Short sale is a sale by the homeowner with the permission of the lender, while foreclosure is a legal process initiated by the lender after missed mortgage payments. - What is the impact of short sales and foreclosures on credit scores?

Foreclosures cause a more significant drop (100-160 points) and stay on the report for seven years, while short sales cause a smaller drop (50-120 points) and stay on the report for four years. - Can I buy another residence after a short sale or foreclosure?

Yes, but the waiting time is different. A short sale permits a new mortgage in two to four years, whereas foreclosure usually takes five to seven years. - Are short sales and foreclosures taxable?

Yes, forgiven mortgage debt from foreclosures or short sales could be taxable income. Talk to a tax professional. - Can foreclosure be prevented?

Indeed, options are a modification of the loan, refinancing, short selling, or cash sale. The best course may be determined through professional guidance.

HOA estoppel letter is a vital part of any real estate transaction. They provide information to prospective buyers, providing details such as the HOA’s name and contact information, property address, and outstanding financial obligations.

They’re also used by lenders to take real property as security, outlining the terms of the agreement between the lender and the association.

In addition to being an important document in real estate transactions, they’re also used by parties involved in a dispute over association fees or dues.

HOA estoppel letters are helpful for many reasons. But one of the most notable is that they help ease the transition from a current owner to a new one. With this letter, parties involved in a real estate transaction have all the information they would need to know.

Essentially an HOA estoppel letter is used for closing real estate deals and can help avoid potential disputes.

Let’s try to understand more about the HOA Estoppel letter and how useful can it be.

What Is An HOA Estoppel Letter?

HOA Estoppel is a legally binding document that certifies the amount of money a home seller owes to the homeowner association.

The document includes any delinquent amounts due from the seller, any amounts that may be payable to an attorney handling a collection matter on the subject property, and any fees associated with closing escrow.

In some cases, homeowners’ association estoppel letters can serve as the certificate of title for real estate.

In a nutshell, real estate agents and lenders who require additional documentation for loan approval typically use homeowners’ association estoppel letters as proof of title.

Additionally, homeowners’ association estoppel letters are often included in homeowner association closing statements and closing documents when escrow is being facilitated by a real estate agent or lender.

What Does An HOA Estoppel Letter Include?

HOA estoppel letters typically contain information related to homeowner association dues and assessments, such as:

- dates of assessment and payment;

- types of fees assessed;

- total amount due;

- instructions for paying the fees;

and more. In some cases, homeowners’ association estoppel letters include a lien or deed restriction statement that certifies the owner’s current dues and assessment payments.

The HOA should include instructions on how to make payment. It should include a note stating that one cannot add newly discovered debts to an already submitted Estoppel letter.

In general, an Estoppel letter should include a comprehensive overview of the homeowners association’s financial obligations and conditions. I do not believe it should be overly detailed or tedious to read.

It should provide enough information for potential property owners to understand their financial obligations and obligations under the association’s bylaws.

How Does A Buyer Obtain An Estoppel Letter?

To obtain an estoppel letter, a buyer typically obtains one from the homeowners association board through the title search company they are working with.

This letter provides information regarding the seller’s annual fees and any outstanding payments due at the time of sale.

The HOA must provide the estoppel letter. And an authorized representative from the association must complete and sign the document within 10 business days. The association must designate a person or entity with a street or email address for the receipt of a request for an estoppel letter, and this information must be publicly available online.

This information can help buyers make informed decisions about purchasing a property in an HOA jurisdiction. A buyer can also contact the association for additional details about their estoppel letter.

What Happens If The Seller Doesn’t Owe The HOA Any Fees?

If the estoppel letter does not indicate any outstanding fees owed by the seller to the HOA, the buyer is not responsible for any fees belonging to the current owner.

Additionally, the buyer is provided with a warranty deed from the seller. This deed ensures that the title of the property is clear and that the seller holds a clear title to it.

However, the party who demands it must provide the estoppel letter and pay the fee, even if the seller has no unpaid balance.

The estoppel letter ensures no additional costs are associated with purchasing a property with an outstanding HOA balance. It also serves as proof of ownership upon closing. In this way, it provides additional assurance to both buyers and sellers of property with an outstanding balance.

What Does An HOA Estoppel Letter Cost?

The cost of preparing an estoppel certificate normally cannot exceed $299 as of July 1, 2022. If an association receives an urgent request for the estoppel certificate and provides it in less than three working days, it may charge up to an extra $119.00. The association may also impose an extra fee for delinquent accounts, not to exceed $179.

Bottom Line

Homeowners’ associations commonly use estoppel letters to support claims regarding the terms of association agreements.

It typically contains specific facts and information about a particular situation. It can be the date of the agreement, the scope of the agreement, or any other relevant information.

As a buyer, you must get an HOA estoppel letter from the association before purchasing into an HOA. This will let you know if there are any unpaid fees related to a property before closing.

The HOA estoppel letter allows the buyer to take possession of the property free of any encumbrances. It also protects against any claims by the HOA after closing.

An estoppel letter protects all parties and allows you to restart without having to pay someone else’s expenses right away.

When you have extensive support from professionals, real estate transactions become simpler. The goal of New York-based Elite Properties is to simplify the buying and selling process.

For more in-depth guidance on HOA estoppel letters, get in touch now!

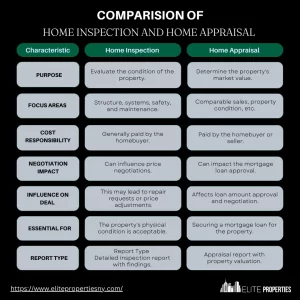

Home appraisal are widely utilized in real estate to establish property worth for a range of objectives. A home appraisal cost plays a crucial role in any transaction, whether you are applying for a mortgage to buy a home, refinancing your current mortgage, or selling your property to a buyer other than an all-cash buyer.

Even without an active real estate transaction, homeowners can benefit from the effort of determining how much to ask for their home on the market or evaluating the financial worth of their estate.

No matter what the purpose is, understanding and considering the cost of a home appraisal is important. So, let us try to understand what a home appraisal is, how much it costs and what factors affect its cost.

What Is A Home Appraisal?

A home appraisal is an assessment of the worth of a home by an appraiser who is licensed or certified to do so. Research into previous sales of nearby comparable homes, a property analysis, current market trends, and the appraiser’s professional opinion support the evaluation.

In simple terms, a house appraisal is a professional’s estimate of the market value of a residential property at a certain time.

Every time a mortgage, refinancing, or sale of real estate is involved, an appraisal is necessary. A home appraisal is an unbiased and objective professional opinion about a home’s value.

The law requires independent, third-party contractors or companies not connected to a bank or lending organization to perform appraisals.

If the transaction involves a purchase and sale of the property, assess the contract price for the home in light of its condition, location, and attributes using the appraisal.

If it is a refinance transaction, the appraisal ensures the lender that he/she isn’t lending the borrower more money than the house is worth.

Why is Home Appraisal Needed?

Understanding the importance of a house appraisal can help you make informed decisions when it comes to buying, selling, or refinancing a property.

- For homeowners, knowing the current market value of their homes can be useful when considering renovations or determining if it’s the right time to sell.

- For buyers, an appraisal can help ensure that the purchase price is fair and that they are not overpaying for a property.

- Lenders rely on appraisals to determine the loan amount they are willing to provide, as they want to ensure that the property is worth the amount being borrowed.

- Appraisals also play a crucial role in the real estate market as a whole. They help maintain the integrity and stability of property values by providing an objective assessment of a property’s worth.

- Without appraisals, there would be a higher risk of overinflated prices, leading to potential financial instability.

What Happens During an Appraisal?

During an appraisal, a licensed appraiser evaluates the property to determine its current market value. Here’s an overview of the typical process:

- Property Inspection: The appraiser physically inspects the property, both its interior and exterior. They take note of the overall condition, features, and upgrades.

- Comparable Analysis: The appraiser researches recent sales of comparable properties (comps) in the vicinity. This helps establish a baseline for the property’s value.

- Property Valuation: Using various valuation methods, such as the sales comparison approach, income approach, or cost approach, the appraiser determines the property’s estimated value.

- Report Preparation: The appraiser compiles a detailed report that includes the property’s description, the methods used for valuation, comparisons with similar properties, and the final appraised value.

- Submit to Lender: In real estate transactions involving a mortgage, the lender orders the appraisal. Once completed, the appraiser submits the report to the lender, who reviews it to ensure the property’s value supports the loan amount.

- Loan Approval Consideration: If the appraised value is lower than the agreed-upon purchase price, it may affect the lender’s decision to approve the loan. Lenders typically want to ensure the property serves as sufficient collateral for the loan amount.

- Negotiation or Resolution: If the appraisal comes in lower than the offer, the buyer and seller may need to renegotiate the sale price, and they might need to find a mutually acceptable solution to proceed with the transaction.

Appraisals are crucial in real estate transactions, providing an objective assessment of a property’s value to protect both the buyer and the lender from overpaying for a property.

How Do I Prepare the House for an Appraisal?

Preparing for a house appraisal can help ensure that you receive an accurate assessment of your property’s value. Here are some steps to consider before the appraiser arrives:

- A clean, clutter-free space can create a positive impression and potentially increase perceived value.

- Fix any minor issues such as leaky faucets, loose doorknobs, or broken light fixtures.

- Pay attention to your property’s curb appeal by mowing the lawn, trimming bushes, and adding colorful flowers or plants.

- Gather any documents that may be helpful during the appraisal process, such as recent renovations, upgrades, or maintenance records.

- Prepare a list of any significant improvements or upgrades you’ve made to the property.

By following these steps, you can present your property in the best possible light and potentially influence its appraisal value.

How Much Does A Home Appraisal Cost?

- The lender typically requests that the appraisal be performed since the appraisal mainly serves to secure the lender’s interests.

- The borrower often pays the fee. However, if the homeowner requests a private appraiser, they become responsible for paying the fee. You can’t negotiate to lower the price because you can’t change the fixed cost of the home appraisal fee.

- The cost of an appraisal can range from $600 to $2,000. But you’ll pay less for a single-family appraisal than a multifamily one.

- Due to their size, multifamily properties typically take longer to appraise, bringing their assessment fees closer to $600.

- A single-family house evaluation typically costs between $300 and $450. However, this can change depending on a variety of factors. These factors include the size of the home, the property’s value, its condition, and so on.

- As mentioned above, a large property will typically cost more to appraise. In bigger cities or in locations where the cost of living is higher the range could be $500 to $800 or more

- The Dodd-Frank Wall Street Reform and Consumer Protection Act regulates professional appraiser fees in part. These rates must be reasonable and customary for the geographic market.

The Appraisal Institute, an association of professional real estate appraisers, recommends that qualified appraisers are licensed or certified in each state and have a good understanding of the neighborhood. Federal regulations stipulate that the appraiser must be impartial. He should be free from any direct or indirect financial interests in the deal.

What Does A Home Appraisal Fee Cover?

A home appraisal fee usually covers the expertise of the appraiser, his/her visual on-site inspection of the home. This involves taking pictures and measurements, the appraiser’s analysis of recent comparable sales. The home appraiser provides the appraisal report summarizing the unbiased assessment of value.

Factors Affecting To The Cost

There are various factors affecting the cost of appraisal. We have listed some common factors below. So, let us jump on to these factors:

- Property Size – If the property size is small, conducting the home appraisal will not take much time. As a result, the cost of the home appraisal will be lower. Similarly, if the property size is larger the appraisal would cost higher.

- Property Type – The type of property also affects the cost of home appraisal. Whether you own a single-family or multi-family house both will affect the cost. A property often costs more to appraise the additional bedrooms and bathrooms it has. Multi-family homes would also probably deviate from the typical sales comparison approach to value estimation, which can raise the price.

- Location – The type of property location also determines the home appraisal cost. Big cities and areas with greater than average living expenses have higher appraisal fees.

- Mortgage Type – Lenders raise the home appraisal cost for jumbo loans. It is because these loans are riskier and not insured or guaranteed. As for the other loan categories, effective from December 2021, the Department of Veterans Affairs increased appraisal fees for VA loans by anywhere between $25 and $400 depending on the region. According to Chase Bank, the typical cost of an FHA loan is the same as that of a standard appraisal.

- Seasonal Conditions – The appraiser may charge you more during certain times of the year if the situation makes it harder for them to access the property.

What Negatively Affects a Home Appraisal?

During a home appraisal, it’s important to avoid common mistakes that can negatively impact your property’s value. Here are some mistakes to avoid:

- Be transparent with the appraiser, trying to hide or downplay issues can lead to an inaccurate appraisal.

- Restricting access to all areas of the property can hinder the appraiser’s ability to accurately assess the property’s value.

- Avoid emphasizing personal preferences or subjective opinions during the appraisal.

- Neglecting maintenance, such as peeling paint, leaky roofs, or broken windows, can negatively impact the property’s value.

- Don’t overlook essential structural or mechanical improvements, while cosmetic enhancements can improve the appeal of your property.

Avoiding these common mistakes can help ensure a fair and accurate appraisal of your property’s value.

Bottom Line

Home appraisals can help understand the financial value of a home for making informed decisions.

Any situation you come across while buying, selling, or refinancing a property would benefit from having a basic understanding of how home appraisals works and how much they cost. The cost of home appraisal varies depending on factors such as the size and complexity of the property.

Get an appraisal from a qualified professional appraiser for accurate and reliable information on your home’s value. Connect with us today for more details!

FAQ

Who pays for a home appraisal?

In real estate transactions, the appraiser is appointed by the buyer’s mortgage lender and the homebuyer pays for it. It is one of the buyer’s many closing costs.

Under federal law, neither the buyer nor the seller selects the appraiser. The lender is barred from working with the appraiser to ensure a fair, impartial appraisal of the home.

What happens if the appraisal is lower than the offer?

If the home appraisal cost is lower than the offer, the lender won’t approve the loan.

In such circumstances, buyers and sellers need to come to a mutually satisfactory solution that will hold the deal together.

How to find a reliable appraiser?

Finding a reliable appraiser is crucial to ensure an accurate and unbiased assessment of your property’s value. Here are some tips to help you find a reputable appraiser:

- Ensure that the appraiser is certified by a recognized professional organization, such as the Appraisal Institute or the American Society of Appraisers.

- Seek recommendations from real estate agents, lenders, or friends who have recently had their properties appraised.

- Use online directories or search engines to find appraisers in your area.

- Contact multiple appraisers and ask them about their experience, qualifications, and fees.

Remember to choose an appraiser who is knowledgeable about your specific property type and location. A well-qualified appraiser can provide a more accurate assessment of your property’s value.

What are the alternatives to traditional house appraisals?

While traditional house appraisals are the most common method of determining property value, there are alternative methods available. These alternatives can be useful in certain situations where a traditional appraisal may not be feasible or necessary. Here are a few alternatives to consider:

- Automated Valuation Models (AVMs): AVMs use algorithms and data analysis to estimate a property’s value based on factors such as recent sales data, property characteristics, and market trends.

- Broker Price Opinions (BPOs): BPOs involve a real estate agent providing an opinion of a property’s value based on their knowledge of the local market.

- Comparative Market Analysis (CMA): CMAs are commonly used by sellers to determine a listing price but should not be considered as precise as a traditional appraisal.

While these alternatives can be useful in certain situations, it’s important to consider their limitations and consult with professionals to determine the most appropriate method for your specific needs.

You are preparing yourself to close the deal and enjoy the proceeds through the property sale. On the other hand, the buyer just wants to move into his or her new home.

But, guess what?

The landscaping of the home is incomplete or maybe some significant repairs to it are yet to be done.

There is trouble and you really do not want the closing date to be pushed back.

Well, you need not! As you can definitely close on time by requesting an escrow holdback.

If you have never sold or bought a house before, you probably might not be familiar with this real estate term called escrow holdback.

But we have got your back, so let’s dive into understanding what escrow holdback is and how it helps you sell your home on time.

What Is An Escrow Holdback?

In the property selling process, there could be times when the house might not be yet ready, despite the nearing move-in date for the buyer, and this may also put you under the pressure of closing the deal on time.

Similar to this, there are times when a builder or contractor delays completing a new home as the move-in date draws near.

However, the closing can still be done with the help of an escrow holdback, which entails money set aside to reassure the buyer that the seller or contractor will complete specific work at a later date.

In simple words, an escrow holdback is a legal arrangement where a sum of money is kept in an escrow account that is owned by a third party. A holdback escrow account is funded by the seller’s portion of the closing proceeds.

An escrow account is a third-party account where money is held until the specific transaction is finished in accordance with predetermined terms. Its main function is to shield buyers from project delivery delays and sellers from late payments.

A sufficient amount of cash must be kept in the escrow account for the seller or contractor to encourage them to complete the project and prepare the home for the buyer’s move-in.

What Is An Escrow Holdback Agreement?

An escrow holdback agreement will state that a portion of the selling proceeds will be kept in an escrow account, usually by a closing attorney, while repairs or renovations are made.

These holdbacks can be applied to certain defects in the property, including unfinished construction work.

For instance, if a seller lacks the money to buy a new septic system for the home, as per the agreement the repairs could be funded by using a certain portion of the sales proceeds. The sum designated for installing the septic system will be retained by the escrow holder.

The seller will not necessarily have to pay for the work before receiving the proceeds from the sale of the property. Also, an appraiser may occasionally need to look through the work required to request a holdback.

To bring the escrow agreement into action, your lender must approve and sign it at closing. Both you and the buyer must sign the agreement before it can be submitted to the lender.

How Does Escrow Holdback Work?

An escrow holdback begins with an addendum to the real estate contract. It specify the repairs that must be completed, their anticipated cost, a completion date, and the method of payment for the seller or contractor.

Further, the escrow holdback agreement must be signed by both the buyer and the seller. This is done before it can be presented to the lender. If the escrow holdback is permitted by the loan underwriter. The lender will either work with a title company to set up an escrow account or take care of it internally.

With some exceptions, the seller is often obligated to provide the funds for the escrow holdback. The account will be filled with the proceeds from the sale of the property if the seller needs to sell the house to pay for the repairs.

The lender will generally demand that the account balance of an escrow holdback be greater than the expected repair costs.

The additional funds are set aside in case the project’s repair costs rise. Besides, repairs must be finished in a predetermined amount of time.

Lastly, comes the verification part. A final inspection is performed once repairs have been made to the property. It is to ensure that the work has been completed. The escrow account will release the funds if the repairs are accomplished promptly and satisfactorily.

What Reasons Qualify For Escrow Holdback?

For exterior repairs that an appraiser deems necessary, an escrow holdback can be employed. Usually, escrow holdbacks can cover the driveway, deck, fence, landscaping, porch, sprinkler system repairs, pest control, lawn seeding, and so on.

You must finish interior improvements and repairs necessary to ensure the property’s health, safety, and habitability before closing. They are not eligible.

In a nutshell, escrow holdbacks cannot be used for all home repair issues. Lenders generally won’t fund a property with safety and health issues. Typically, escrow holdbacks are used for outdoor or weather-related problems.

Bottom Line

The process of collecting funds from the seller’s proceeds at closing, known as escrow holdbacks. This will return the funds once the property has undergone the required repairs or improvements.

It reassures you that the buyer is committed to the purchase. On the other, the buyer gets the money, if the repairs aren’t completed on time.

Escrow holdbacks are a common occurrence in the real estate market. You can consider requesting an escrow holdback from your lender if necessary repairs are putting your closing date in trouble.

If accepted, it might help you make the repairs quickly and keep your real estate transaction on time. And the selling process smooths enabling you not to push back the closing date. Your lender can assist you in understanding the escrow holdback procedure.

You can also seek advice by getting in touch with Elite Properties today!