Adverse possession is a legal guideline when someone obtains the title of another person’s property or land. Elements of Adverse Possession and their Rules differ by jurisdiction. But usually, somebody can claim adverse possession after they’ve taken up residence on or have uninterrupted ownership of a piece of property for a definite amount of time.

In this blog, we help you learn more about what is adverse possession, the legal norms for that classification, and how it could affect you as a property owner.

What is adverse possession in real estate?

Adverse possession endows possession of land to someone apart from the owner if that person inhabits it for longer than the order of limits for that jurisdiction. Adverse Possession is a strange law where someone occupies property without permission. Also, then acquires a legal right to that property once a set amount of time has passed.

What are the 5 requirements for Adverse Possession?

The requirements for asserting an adverse possession claim vary from state to state, but there are two main reasons why these requirements exist.

- The first reason is to give the rightful owner of the property a chance to stop the adverse possessor from taking over through several different methods.

- The second justification is that adverse possession allows for the property to be put to good use instead of sitting unoccupied and undeveloped.

Understanding the requirements is crucial for individuals seeking to claim ownership of property through statutory ownership. To address the query, “What are the 5 requirements for adverse possession”, a legal concept in real estate, entails five essential conditions:

- Open and Public: Adverse possessors must be using the property openly and notoriously. This means that the user cannot be hidden from view. This would allow the true owner to see the use and stop it. If the adverse possessor’s use is happening in secret, the owner may not learn of it until it’s too late to assert their own rights.

- Hostility Claim: The claim of someone who uses adverse possession must be against the owner’s use of the land. This means that the adverse possessor may not make an adverse possession claim if the owner permitted them to use the land.

- Continuous Possession: To qualify for adverse possession in New York, the trespasser must have had exclusive and continuous possession of the land for at least ten years. This means that they cannot have left the land for any significant periods during those ten years.

- Actual Possession: The individual must physically occupy the property and use it as a true owner would. Mere intentions or occasional use are usually insufficient; there must be tangible occupation.

- Exclusive Possession: The possession must be exclusive to the adverse possessor and not shared with the true owner or others who also claim ownership rights. Joint use with the owner typically doesn’t qualify.

Also, one additional requirement is Time Period. All states have a time limit in which the adverse possessor must use the land before it officially becomes theirs. In New York, the law requires that land must be used for a minimum of ten years before the adverse possessor gains title to the property.

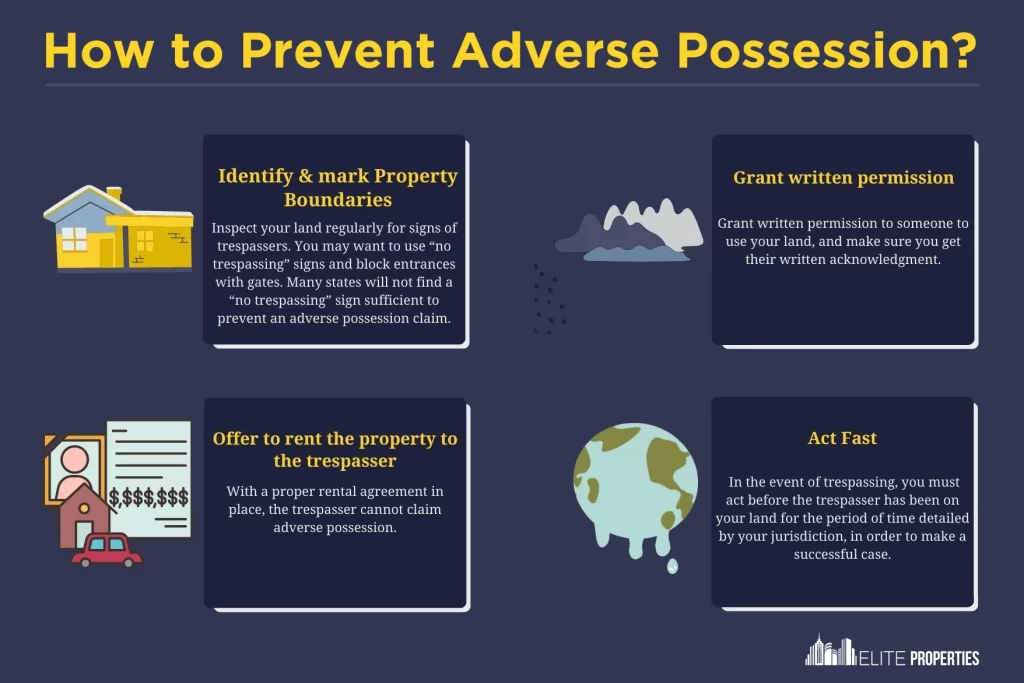

How to Prevent Adverse Possession?

- Regular Property Checks: Conduct regular inspections of your property to identify any unauthorized use or occupation. Attention is key to catching potential adverse possessors early on.

- Maintain Clear Boundaries: Mark your property boundaries with fences, walls, or signs. This helps to establish the limits of your property and discourages encroachment by others.

- Document Property Use: Keep detailed records of your property use, including maintenance activities, improvements, and any notices sent to potential encroachers. This documentation can serve as evidence of your active ownership.

- Communication with Neighbors: Encourage open dialogue with neighboring landowners to resolve boundary concerns promptly, preventing potential misunderstandings that could result in occupancy claims.

- Regular Property Use: Not only consistently utilize but also maintain your property according to ownership rights. Active involvement with your land strengthens your ownership claim also minimizes the chance of others claiming encroachment.

- Legal Action When Necessary: If you discover unauthorized use of your property, swiftly pursue legal steps to resolve it. This could mean issuing warnings, bargaining boundary agreements, or taking legal action such as eviction or trespassing charges.

- Monitor Legal Deadlines: Stay informed not only about the legal timeframe for prescriptive rights in your area but also the act ahead of time to avoid it. Consistently monitor your property and promptly address any potential claims to safeguard your ownership rights.

In What Way Does It Work?

Adverse possession is when a non-owner/trespasser/squatter inhabits real property deprived of consent. The owner must attempt to do away with them during the ruling of limitations period; otherwise, the person obligating the possession could possibly take legal ownership. However, for there to be adverse possession, each of the following criteria must be met

- Exclusive and continuous: The possessor has to have persisted on the property uninterruptedly, without others inhabiting it as well.

- Actual possession: The person must tangibly inhabit the property, not just mention that they want to control it.

- Hostile possession: The possessor, by inhabiting the property, is trespassing on the original owner’s rights without consent.

- Open and notorious possession: The possessor is not nagging onto the property. Not only they are amenably living there in a way an owner would, but also their occupation should be evident to any outside observer.

How to File for Adverse Possession

It’s crucial to understand the laws as well as procedures governing squatter’s rights in the relevant area and possibly seek legal advice to ensure compliance and increase the chances of a successful claim. Here’s what you should know about how to file for adverse possession:

- Consult with a real estate attorney: An attorney can assess your situation, determine if you meet the requirements for statutory occupancy in your specific jurisdiction, and guide you through the filing process.

- Gather evidence: You will also need documentation to prove you meet the five requirements for a claim of right. This might include things like property tax bills addressed to you, receipts for repairs or improvements made to the property, and affidavits from witnesses who can verify your exclusive and continuous use of the land.

- File a lawsuit: With your attorney’s help, you’ll need to file a case against the legal owner of the property. This case will initiate the legal process of claiming ownership through prescriptive rights.

Examples of Adverse Possession

Adverse possession can take place in a couple of ways.

- First, adverse possession could be granted to someone who purposely occupies property that doesn’t belong to them. Such as a trespasser or a squatter, who lives there for a long period of time. This may take place in the case of an absentee owner not checking on the property. If enough time passes per the state’s law, the title is transferred to the trespasser.

- The sum of time necessary to inhabit a property before initiating the its process differs by state and local law, usually taking more than a few years.

- Somebody could meet the requirements for adverse possession in as little as two years in Maricopa County, Arizona. Even though it’s more likely to see longer periods, for instance, 10 years in New York.

- In another mundane example of it, somebody such as a neighbor intrudes on a rightful owner’s property. For example, a neighbor may construct a garage or build a fence that crosses a property line. This at times is done unintentionally, but it could result in adverse possession. It’ll happen if the infringement occurred for long enough.

You can also go through the Laws of Adverse Possession of New York, to know more.

What Is the Time Limit on Adverse Possession?

The time limit for adverse possession, also known as the statutory period. It is the critical duration someone must occupy another’s property to claim ownership through squatter’s right. Also, it’s a key factor and varies depending on your location. Here’s a breakdown:

- No Single Time Limit: There’s no one-size-fits-all time limit across different countries or even states within a country.

- Range: The statutory period typically ranges from 3 years to 30 years.

Who Can Claim it?

In general, anyone who meets the legal requirements for encroachment can claim ownership of another’s property after a specific period. However, there are some limitations and exceptions to consider:

- Individuals: Any individual can potentially claim possessory title if they meet the requirements.

- Government Entities: In some cases, government entities like municipalities or states might be able to claim statutory ownership, but the rules may differ.

- Successors and Heirs: The rights to an adverse occupancy claim can sometimes pass to successors or heirs of the original possessor if they continue meeting the requirements.

Difference between Adverse Possession and Homesteading

| Aspect | Adverse Possession | Homesteading |

| Legal Basis | Based on occupancy without the owner’s permission | Based on government grants or laws |

| Intent | Does not require permission or intent to own | Requires intention to establish ownership |

| Ownership Transfer | Acquired by continuous use without owner’s consent | Acquired through government grant or specific laws |

| Duration | The statutory period of occupation varies by jurisdiction | Typically involves a fixed period of residency |

| Purpose | Often occurs unintentionally or through negligence | Intentionally seeks to establish ownership and settle |

| Requirements | Continuous, hostile, open, exclusive, and notorious possession | Compliance with government regulations and residency |

| Examples | Squatting on unused land without permission | Settling on public land under homesteading laws |

Bottom Line

Adverse possession can result in a legal headache for a property owner, but there are means to escape it. The best constraint for illegal inhabitants is to keep consistent tabs on a property. Ensure that there is a lock on everything and is fence-proof.

If the owner grants written permission to trespass on their property, then it would not be adverse possession. Still, be careful that permitting a neighbor to build on and/or encroaching on your land. They could cause problems if and when you try to sell.

Should you find yourself in a situation in which someone is on the verge of qualifying for adverse possession, hire an attorney to assist you in filing a lawsuit to remove the party and/or reclaim the property. Additionally, refer experts from Elite Properties who can assist you in making the right decision. We are a cash buying company that suggests we provide fast closings. Call us at 718-557-9261 today.

FAQ

1. How many years is adverse possession in NY?

Adverse possession in New York requires a continuous occupation of at least ten years to establish a claim to ownership of property. This duration is subject to specific legal requirements outlined by New York state law.

2. Can adverse possession be challenged?

Yes, it can be challenged through legal means. Such as filing a lawsuit to dispute the adverse possessor’s claim to the property. Challenges may involve proving that the holder neither meet all the necessary legal requirements nor demonstrating continued ownership and control of the property by the original owner.

3. What are the 5 main elements to obtain an adverse possession of a property?

The five main elements to obtain adverse possession of a property include continuous and uninterrupted possession, open and notorious use, hostile or adverse occupancy without permission, exclusive possession, as well as the statutory period of occupation, which varies by jurisdiction.

4. Does adverse possession apply to new owners?

Adverse possession laws can apply to new owners if the conditions are met. Regardless of whether they acquired the property through purchase or inheritance. However, new owners may have legal recourse to challenge claims if they can demonstrate continued ownership and control of the property.

5. What are two options to avoid adverse possession?

To avoid adverse possession, property owners not only regularly monitor their land but also address any unauthorized occupation promptly. Additionally, maintaining clear boundaries and actively using the property. Also, this can help prevent hostile possession claims from arising.

6. What is the shortest time for it?

The shortest time for it varies by jurisdiction but typically ranges from a few years to several years. However, not only specific legal requirements but also the conditions must still be met within this timeframe for encroachment to be established.

Introduction

For the majority of people, home purchasing is the biggest purchase. A detailed and attentive approach will suit you well when it comes to purchasing real estate where you’re going to devote a major portion of your time.

Once beneath contract, the classic timeline is nearly 40-50 days to close on a home. Let’s bear in mind the steps are taken up to that point—house hunting, pre-approval, and application process. Whether it’s your very first home, a renovation from a starter home to something bigger, or scaling back after several years, you shouldn’t hurry the process.

Here are the Nine Steps with an approximate number of days to complete home purchasing:

1. Look for an agent (7 days)

The majority of us are in touch with a friend, family member, or colleague who newly purchased a home. Enquire from those trusted sources, and in nearly a week you should be in a position to contact a trustworthy agent. You’re in search of someone you like, have faith in, and who has a well-informed hold on the available inventory in your preferred community. A good agent should assist you in avoiding a bad purchase and see you through the ifs and buts of sealing the deal.

2. Acquire Mortgage Pre-Approval (8-10 days)

Loan pre-approval is needed and will let you know if you are qualified for a mortgage. You’ll need documents comprising tax returns, pay stubs, debt, and credit information, and if you’re purchasing with the other half or partner, you’ll both require these things. You can also check with several lenders to check for the ideal rates. At the time of the pre-approval process, there’s a 14-day window during which credit bureaus consider credit inquiries as a single one since you’re purchasing a home.

3. House-Hunt (80-85 days)

Many people regard real estate as an obsession and like to look at real estate trends in several areas around the country comprising what homes are selling for, and how much home you can avail for your dollar, but when you’re truly in the market to buy, house-hunting isn’t always the most amusing.

You may be hassled, stressed to confront, or require to make the purchase well within time to relocate your family or get the kids stable before school begins. A study conducted by Insight Media established it takes nearly 81 days to surf homes prior to finding one to buy. And a major chunk of people views roughly 16 homes online before finding one they desire. The average time required to search prior to scheduling a visit? Twenty hours.

As per the study, 14% of individuals said they had to find the middle ground on some features of their dream home. And in the present seller’s market where homes in various areas of the country get many offers over the inquiring price or have a bidding war, a quarter of home buyers or more may involve an unsuccessful offer delaying their home search.

4. Get Final Approval for Mortgage to Home Purchasing

Just because you’ve gotten pre-approval for your mortgage doesn’t mean that you’re immediately locked into that loan for the home you have under contract. The lender has a few more hoops for you to jump through, such as an inspection and appraisal of the home. They’ll also want to see more current copies of your financial documents.

From this point on, the steps to buying a house will often overlap. This means you’ll have several things in the air as you move forward with the purchase.

5. Put Forth an Offer (5 days)

You’ve finally found the house and now all you are required to do is put forth an offer. Your agent will clarify everything you need to be aware of but essentially, if you and the agent agree on the price you’re proposing, you’ll want the standard 1% earnest money. And above, in a tight seller’s market, you may want to knock that up to 3-6% to show you’re playing for keeps. You could also contain a personalized letter to the owner telling them how much you love the home and why you’re interested in their house.

6. Get a Mortgage (21 days)

Your offer is accepted! Now the mortgage procedure begins. Although the lender you have chosen can lock in your interest rate, you’re about to cross more hurdles and collect more documents such as current bank statements and work stubs for the concluding mortgage documents. Lenders will also need an appraisal and inspection and go through the extensive list of final expenses and estimate yours.

This process can include anywhere from a few weeks. In this tie, you can communicate with your lender via email or phone every couple of days with a new request. You have to submit your inspection and appraisal reports to the seller. If any of them has any discrepancies, you have to renegotiate the price, and make repairs. There will be a title search to ensure the home is free and clear of liens. You’ll likely select homeowner’s insurance and offer the lender all the data. Your insurer might even need a pre-inspection prior to insuring you. After your mortgage is pre-approval, there is still a lot of work to do.

7. Close on the House (50 days)

On the day before closing or the day before, you should take a final stroll. Make sure all repairs are complete and there is no damage. Your lender has probably told you how you must pay closing costs. It may be to bring along a cashier’s check or how you’ll make a digital transfer of the money. You’ll also require a photo ID and a nice pen for the whole bunch of documents you’ll be signing. At last, the keys are handed over to you and congratulations are in place. You’ve bought a home.

8. Homeowners Insurance

Insurance companies usually send out an inspector to check for any risks that the property might have. This process might take a few days. In addition, the mortgage lender might require other types of insurance, such as flood insurance.

After this, the process of buying a house often overlaps with other steps.

So you’ll have multiple things going on at once.

9. Ready for Closing Funds

Your agent will let you know whether you should bring a cashier’s or certified check or transfer funds digitally to release the money. If you get wiring instructions by email, call your agent or lender to confirm one of them sent it. Use the phone number you have on record for your agent, not the one in the email.

Which step of the home purchasing process is the most lengthy?

Hunting for your dream home is probably what takes the most time. Scheduling, setting a budget, and determining what things you’ll compromise on in advance can help make the process smoother.

What facts should you take into consideration while house hunting?

While every situation is distinct, one of the key things people look for is a good site. You may desire that the property be located conveniently for work or school, or possibly you simply prefer a definite area.

Other facts many people find useful to note are curb appeal, the size and layout of the home, the number of beds and baths, and the placement of windows for natural light.

What are the few red flags to take note of when home purchasing?

Try to figure out big cracks in the driveway, foundation, or walls. The home shouldn’t feel moist inside or have a stuffy odor. Look for cracked paint on window frames. Staging furniture and baking smells may deceive you.

Bottom Line

Home Purchasing is a complicated and stressful process. The better equipped you are for each step, the better your odds are of arriving at a good home. So what are you waiting for? Gather your documents, choose a realtor and insurance provider and begin your home purchasing journey. Make sure to study real estate trends in your area. Additionally, refer experts from Elite Properties who can assist you in making the right decision. We are a cash buying company that suggests we provide fast closings. Call us at 718-977-5462 today.

Are you on your move to the home selling process? If yes, you may be enticed to go beyond updates and improvements. You may want to fetch the peak price across the table. Some improvements that add value to your home include substituting your garage door or carrying out a slight kitchen remodeling. Although, others offer hardly any opportunity to pull through the expenses when it’s a stint to sell.

So, here are

6 things you believe to enhance your home selling process, but actually, don’t.

#1 Swimming Pool

A big swimming pool may sound like a dream, but it’s a costly affair. It could be one that may not offer any monetary return. In specific cases, a pool might add value to your home, but it may not essentially make it cost-worthy. Sources state a pool can enhance your home’s value by up to 7%, but only if –

- You are living in an upmarket neighborhood where pools are the protocol

- The elegance of the pool suits the neighborhood

- You are living in a hot climate where you can make use of the pool around the year

- The pool doesn’t cover up the complete yard and you still have room for sports or gardening

- The pool is in good condition

- You can appeal to the exact buyer—for example, families with small children may be worried about security issues, but elder grownups or individuals without kids may adore the idea of a pool

Else, think of a pool as an outlay in your lifestyle, but don’t imagine it to be an investment in your home.

#2 Overbuilding for the sake of Neighborhood

At a certain point in time, you may require more room but don’t wish to undergo the trouble of moving. Possibly you want an additional bedroom for your budding family or an office back home. Certain enhancements may involuntarily make your home stretch beyond the norm for the neighborhood. A huge, affluent remodel may let the home become more enticing. For instance, opting for a second story with an additional bedroom and a full bath. It won’t enhance the resale value in case the remaining neighborhood homes have small, one-story homes.

#3 Unreliable High-End Renovations

Improvements should be constant all over the home. Stainless steel gadgets in your kitchen or imported tiles in the entryway will hardly do anything to raise the value of your home. If the bathrooms still have vinyl floors and the carpet is an old shag it won’t justify the home’s worth. Remodeling may not fetch a higher return except the rest of the home matches up to the same level. High-quality advancements usually raise the value of high-end homes, but not essentially in mid-range houses where the improvement may be uneven with the rest of the home.

#4 Unseen Improvements

Unseen improvements are expensive developments that you envision to make your house a superior place to live in. But having said that not one person else will recognize or likely take care of it. You might require a brand-new plumbing system. Yet, don’t imagine recuperating the costs when it’s time to sell. The majority of home buyers assume these systems to be in upright working condition. They will not shell out even an extra penny, simply because you recently mounted a new heater. It is a better option to consider these improvements as part and parcel of regular maintenance if you want to sell your house fast. Don’t count them as an investment in your home’s value.

#5 Wall-to-wall Floor covering

Real estate listings may suggest new carpeting all over as a selling point although homebuyers may flinch at the idea of having floor covering. Most people are moving away from carpeting as the chemicals are needed to process it. Not to state its potential for catching allergens—a grave concern for people with children.

#6 An Extended Owner’s Suite

A brand-new owner’s suite with a lavish bathroom and walk-in wardrobe can be a big USP that escalates your home’s value. But said that it does not essentially is the case if the remodel turns your prim and proper three-bedroom home into a stuffy two-bedroom home.

Bottom Line

If you’re planning for home improvement, it’s beneficial to boil down and understand if an upgrade is something that you will cherish, or if you’re just putting in the effort to increase your home’s value. If a swimming pool is something you would make use of and relish for several years, you may be capable of justifying the cost, even if you don’t recover your hard-earned money. Conversely, if you consider spending thousands of dollars just to remodel and hike your home’s sale price, you’d better rest assured that your money is well spent.

When dubious about the home selling process, equate features of equivalent homes in your neighborhood. Make sure to study real estate trends in your area. Additionally, refer experts from Elite Properties who can assist you in making the right decision. We are a cash buying company that suggests we provide fast closings. Call us at 718-977-5462 today to sell your house fast for cash.

Need to sell your house fast, but don’t know how to negotiate the prices? This is an obstacle every homeowner faces while thinking about selling their homes. As it’s one of the biggest financial transactions you’ll need to think about various points before actually selling it. Several factors come into play while you work on pricing your home. Factors like commissions, closing costs, etc. make up for the final price hence, you may want to consider negotiating. You can use these negotiating strategies to sell your house fast.

Oppose at Your List Price

As a seller, you will never accept an offer that’s less than the asking price. Potential buyers usually look for a back-and-forth negotiation that ultimately results in settling for a lower price. In this case, the seller usually makes a counteroffer that’s a little higher, but still below the listing price. The seller counteroffers because they fear losing a potential buyer. Applying this strategy will surely help you close the deal. As this is a possible way to sell your house fast it won’t give you maximum profits.

Here, instead of dropping the price, you can stick to your listing price. If there’s a buyer who really wants to purchase the house then they will come back with a higher price. Although, the buyer will only come back if you’ve set a fair price for your house.

Repudiate the Offer

If you consider yourself bold enough you can try another negotiating tactic which is rejecting the offer. Rejecting means you won’t be able to make a counteroffer at all. If you want the buyers to still be in the game you can ask them to submit a new offer. If they still want the house and you haven’t put them off, they might come up with a new offer. This strategy will require you to be strong on your verdict. Also, you must be able to justify the property’s worth.

When you reject an offer you are not legally barred from a negotiation with a particular buyer. You can accept a higher offer if it comes along. When a buyer knows there can be another buyer with a better offer it automatically creates pressure to resubmit quickly. Furthermore, this strategy only works if your home has been on the market for a short duration or if you have an open house.

Add an Expiration Date on Your Counteroffer

Let’s say a buyer submits an offer that you don’t want to accept and you counter their offer. If this happens, you’d be in terms of negotiation with that particular buyer. In this case, it’s unethical to accept a better offer from another buyer although it’s not illegal. It is possible for you to be a part of multiple negotiations with multiple buyers. Eventually, it’s the seller’s prerogative to disclose or not disclose information to the prospects.

A seller can legally counter more than one offer but they must include suitable language considering the situation. With a will of selling your house fast, you may want to put an expiration date on the counteroffers. Also, be considerate of the deadlines, since a short duration may result in a turn-off for the buyer. If the default expiration is four days you can shorten it by three days.

While you have an outstanding counteroffer, your home is off the market. Most of the buyers won’t submit an offer if the other one is on negotiating terms. Here, if the deal falls through, you’ll be adding more days to your home sitting on the market. If your home exceeds a certain amount of time it becomes less desirable to buyers. So, adding an expiration date to your counteroffer will push buyers to make a faster decision.

Accept to Pay the Closing Costs

Nowadays, it has become a practice for sellers to ask for closing costs. The closing cost can anywhere be up to 3% of the buying price. While paying the closing costs buyers usually feel cash-strapped. Paying moving expenses, down payments, improvement costs, and even closings can make a hole in their pocket. Sometimes buyers can’t afford to pay the additional closing cost without assistance.

When a buyer submits an offer and asks the seller to pay the closing costs, you can counter it by asking for a higher purchase price. This can also translate into asking for a higher price than the initial purchase price. Usually, buyers fail to realize when they ask sellers to pay the closing cost they’re actually lowering the home’s worth. The catch is, if you increase the asking price post paying the buyer’s closing cost you’ll still end up with a good amount.

Bottom Line

The way to successfully execute these negotiation strategies is to have an excellent product that justifies its price. Your home must be in a spotless condition and you must be able to make fast decisions. If you want to sell your house as-is and want to avoid negotiations then get in touch with Elite Properties. We are a cash buying company which means we offer fast closings and a no-obligation offer. Call us at 718-977-5462 today to sell your house fast for cash.

Introduction

Mortgage deferment and forbearance are two options for homeowners that help in temporarily lowering their monthly mortgage payments. The major difference between these two options is whether the interest accrues and the time for repayment. Here, we will be talking about the difference between mortgage deferment and forbearance. There are multiple aspects when it comes to these methods like payments, interest, etc.

What’s the Difference Between Mortgage Deferment and Forbearance?

- Payment Assistance– In a mortgage deferment, the mortgage borrowers can delay past payments during the forbearance period. They can furthermore repay them at the end of the loan’s tenure. Here, as your mortgage payments are deferred, you are required to pay your monthly payments on time. Furthermore, forbearance pauses or reduces payments for homeowners suffering from financial hardships for a certain amount of time. Although the borrower has the option to make payments during the forbearance period, it’s not obligatory. In some cases, lenders may require the borrower to provide regular updates on their financial transactions during the forbearance period.

- Interest Accrual- In an interest accrual, the mortgage payments that have been deferred to the end of the loan’s tenure don’t accrue additional interest. Whereas, in forbearance, the interest accrues each month as scheduled.

- Repayment – Concerning repayment, in forbearance, you may have to catch up on the past payments post the forbearance period ends. Although, this depends solely on the loan and forbearance terms. For example, if your monthly payment structure is $1500 and you apply for 6 months of forbearance. You’ll owe $9000 towards the end of forbearance. Furthermore, deferment allows you to delay missed payments in case you sell your house or refinance.

What’s the Right Choice for You?

A deferment can be an ideal choice for you if you’ve come to the end of the forbearance period. You may benefit from deferment if you have just ended a period of forbearance. Also, if you are able to resume monthly payments but cannot afford to make up the payments missed during forbearance. This applies even to a repayment plan. Moreover, if you do not wish to permanently modify the loan terms you may be able to opt for deferment.

On the other hand, forbearance can be the right choice for one who is experiencing a brief period of financial hardship. This can be inclusive of job loss, illness, or any kind of disability. Here, you will have to provide proof stating the reason for the crisis.

Additional Information

COVID-19 may affect your ability to repay the outstanding payments. Although, under the CARES Act, you are able to request forbearance without providing documentation. If your loan is backed by either of the departments given below. You must have been requested an initial forbearance by September 30, 2021.

The departments are as follows-

- Department of Housing and Urban Development (HUD)

- Federal Housing Administration (FHA)

- United States Department of Agriculture (USDA)

- Department of Veterans Affairs (VA)

Furthermore, Fannie Mae and Freddie Mac do not impose a deadline for asking for an initial forbearance on your loan. Borrowers with federally backed mortgages won’t have to make a lump-sum payment at the end of the forbearance. Considering the COVID-19 adversity. Additionally, these borrowers will be eligible to defer the pending payments for up to 12 months.

The Bottom Line

According to the information above the conclusion is that forbearance provides momentary relief to homeowners suffering from the financial crisis. Although, at the end of the forbearance payments the monthly payments must be given in full. In such instances, homeowners may consider having deferment to postpone the one-time amount until the end of the loan’s tenure. Moreover, if you want to avoid the hassles and sell your house you can contact Elite Properties. We are a cash buying company which means we can help you sell your house fast for cash. Call us today at 718-977-5462 and sell your house in any condition and location.

An open house or a walkthrough is a time when potential buyers can visit the property for a viewing. This usually occurs when a broker asks the owners or renters to vacate the property in order to keep it vacant for others to see and evaluate the space. An open house can also be seen as a way of advertising the property to attract more buyers. If you are a homeowner and considering keeping a walkthrough, keep reading about what is an open house.

How Does An Open House Work?

In real estate, trading properties is an example of a relatively illiquid market consisting of diverse products. Each property will be different from another even if they co-exist in the same neighborhood. The process starts by vacating the property post which the seller or the seller’s agent allows the buyers to enter and have a walk through the place. The house tour proceeds with the real estate agent’s assistance or the seller’s if it’s an FSBO.

The motive of a walkthrough is to offer an ample amount of time to buyers and secure their interest. They additionally get a chance to evaluate the home as well as the surrounding area. Also, it’s always a better idea to attend an open house instead of booking a brief appointment with a broker. Open houses are often set up on the weekends. Sundays in particular, the reason being the availability of maximum people. Furthermore, some owners or agents make it fun by serving coffee, drinks, or hors d’oeuvres at a walkthrough event.

Pros and Cons of Open Houses

For people who want to sell houses fast, an open house provides the opportunity to attract buyers. A good set-up event can interest more buyers leading to a profitable offer. Real estate agents often suggest that homeowners keep an open house on the first-weekend post after the property goes up for sale. As beneficial as it sounds, a walkthrough has certain pros and cons. Some sellers say open houses are too much work, sometimes even more than the house’s worth.

Here are some pros and cons of an open house that you may comprehend

Pros

- Entices curious buyers

- Alerts the real estate agents about the issues with the house through visitor feedback

- May steer to an immediate offer

Cons

- Can involve more effort in organizing than the house’s worth

- Online listings can get more potential buyers in less time

- Homeowners need to leave their homes during all open houses

As a homeowner, you must leave the property for other people to view it. This means you’ll have to make arrangements for pets and children if any that will cost you a lot. Owners also need to remove personal belongings to deter buyers from imagining themselves in the house. Additionally, it also means safeguarding your personal stuff that can be on the verge of theft.

A Broker’s Open House

Unlike the traditional open house, a broker’s open house is only meant for real estate professionals and not the public. A broker’s open house intention is to allow realtors to view the property, and solicit professional opinions and its price. It is also an opportunity for agents to spread the word about a good property and gain clients.

A broker’s open house is often kept on weekdays or midweek when the availability of agents is more. The availability of agents is usually less on weekends as they are busy with clients in walkthroughs.

Bottom Line

Walkthroughs or open houses irrespective of the term, it’s a good way to advertise and sell your house fast. Although, it can take a toll on your head with people constantly visiting your place. Furthermore, managing stays and improvements will definitely cost you hundreds of dollars. If you’re looking for a swift solution and don’t want to compromise on your home’s worth you can get in touch with Elite Properties. We are a cash buying company that offers a fair all-cash offer in any location and under any condition. Give us a call at 718-977-5462 and learn more about the home selling process.

A real estate agent plays a crucial role when buying or selling a home. Buying a home is a big deal hence, paying attention to every detail matters. Additionally, having a real estate agent on your side will help you in eluding multiple issues that come along with the home-buying process. If you’re new to the process then read our blog ‘The Dangers of Buying A Home Without a Real Estate Agent’

Paying Exorbitant Amounts of Money

Unless you don’t belong to the real estate industry you’d hardly know about the accurate prices of homes. Furthermore, if it’s an FSBO home (For-Sale-By-Owner) then, it’s likely that the owner is unaware of the pricing. In most FSBO cases, homeowners overprice the house. Reason being, a lack of knowledge and guidance.

When you hire a real estate agent, they offer you accurate information and provide you with a precise house price. They can give you a fair idea post-first viewing and rest after the completion of CMA(Comparative Market Analysis) or comparables(real estate appraisal term referring to properties with characteristics that are similar to a subject property whose value is being sought.). Additionally, they’ll offer you a suitable bidding price for your house that may take months to establish.

Issues with Disclosures

As a mandatory rule, disclosing problems related to a property is crucial whether it’s for an agent or a buyer. Although, in some places the rules may differ for instance in New York there is a rule known as Caveat Emptor. Caveat Emptor or buyer beware translates that a seller is not entitled to disclose known problems, if there’s an issue then it’ll be on you (seller). Although, major problems like structural issues still need disclosure.

Being Unaware Of The Neighborhood

A good real estate agent will know and understand your needs and the neighborhood that interests you. They will suggest the best neighborhood according to your requirements and value. Furthermore, they will also enlighten you about the market if it’s steep, low, or stable. If you research alone it’s almost impossible to be precise about prices in a city that you’re unfamiliar with. Moving to a new neighborhood is a big deal as you may spend most of your life residing there. Having a real estate agent at your side can identify potential problems in the neighborhood.

Problems while Appraisal

Paying an extravagant amount for a home can be bad, and seeking financing for the purchase is even worse. The case can worsen if you are buying an FSBO home. As none of the sides are represented the buyer eventually ends up paying more. Furthermore, when the home appraisal is run, the bank refuses to approve or sign off as the appraisal value is low and the amount is high. It’s a scary situation as the final price is settled and the seller doesn’t negotiate on the prices further.

Additional Problems

The situations above are some of the nightmares you would want to avoid by not hiring a real estate agent. Adding to the rest there are numerous other risks that you may fall prey to when you try to trade properties.

- Loss Of Time

Researching homes, potential buyers, neighborhoods, and buildings can take a toll on your head. Unless you’re a retired person or are currently unemployed you cannot afford to lose time and property.

- Too Much Paperwork

Real estate agents can be extremely complex with multiple verification processes and paperwork it can get tedious. Laws and regulations can differ from state, city, and region although, it comes inclusive of several documents that require signatures. Every detail counts and if you make any mistake it can cost you a fallthrough or delay.

- Numerous Lost Deals

The real estate market is highly competitive and constantly changing. Failing to make the right move on time can lose you out to other buyers that prepare beforehand. An agent’s job here is to make sure you’re ready to finalize deals and even win buyers/sellers respectively.

Bottom Line

No matter how much you may deny it, hiring a real estate agent will only help you ease the home-buying process. If you don’t have time to deal with a real estate agent you can get in touch with Elite Properties. We are a cash buying company and buy home as-is, we can close a deal in less than a week. This means you can move with the alignment of your timeline without having the need to disturb your schedule. Call us at 718-977-5462 and get to know more.

Private Mortgage Insurance (PMI) is a policy that protects the lender or the lending institution if you fail to repay the loan. PMI covers a part or all of the remaining mortgage, the borrower pays for the policy while the lender benefits. Like other insurance policies, private mortgage insurance comes with an annual premium, and sometimes it also has an upfront premium too. If you want to dive in deep about knowing PMIs, then read our blog ‘Everything To Know About A Private Mortgage Insurance ‘.

What is Private Mortgage Insurance?

Private Mortgage Insurance assures the lender that the loan will be paid, having such a policy helps borrowers to qualify for a loan that they eventually wouldn’t have qualified for. This insurance is mandatory if you pay less than a 20% down payment on a purchase.

In some cases, lenders may allow you to make a down payment of less than 20% without PMI although these loans may have steeper interest rates.

1. How Does Private Mortgage Insurance Work?

Similar to other insurance policies, you pay premiums to cover any unforeseen damages due to unfortunate situations. In such instances, the insurance company is liable for paying the outstanding loan if you find yourself incapable of doing it. Lenders contemplate that it is more likely to happen if you have less of an ownership stake in the property.

2. Private Mortgage Insurance vs. Mortgage Protection Insurance

Private mortgage insurance (PMI) is different from Mortgage Protection Insurance (MPI). Mortgage Protection Insurance won’t pay off the whole outstanding balance of your loan if you default. Although it may still make some payments if you fall victim to uncertain situations like job loss, accidents that led to disability, or any kind of serious illness.

Here are some more insights into both PMI and MPI to help you understand better –

Private Mortgage Insurance

- A PMI insures against a complete default on the loan

- It protects the lender in unforeseen circumstances

- It pays in the event of foreclosure

Mortgage Protection Insurance

- An MPI only covers a chunk or some missed mortgage payments

- An MPI protects the borrower in catastrophic events

- May pay in the event of the borrower’s death

PMI Example

Private mortgage insurance (PMI) is an additional cost that homebuyers may need to pay if they have a down payment of less than 20% of the home’s value. For instance, if you purchase a $300,000 home with a 10% down payment, you could be paying between $1,500 to $3,000 per year in PMI.

To make it more manageable, this cost is typically divided into monthly payments, which could range from $125 to $250 per month in this example. It’s important to factor in PMI when budgeting for your monthly mortgage payments.

Factors Influencing PMI

Amount of Down Payment

When buying a home, the amount of your down payment can have a big impact on your mortgage payments and PMI (private mortgage insurance) costs. If you make a smaller down payment, your lender may see you as a higher risk and charge you more for PMI. This can also lead to higher monthly mortgage payments and a longer time before you can cancel PMI. However, even if you can’t afford a 20% down payment, putting down more money upfront can help lower your PMI costs and save you money in the long run.

Credit Score History

When applying for a loan, your credit history is an important factor that lenders consider. They will review your credit score to determine how reliable you have been in repaying borrowed money in the past.

A higher credit score indicates that you regularly make payments above the minimum amount, borrow within your means, pay bills on time, and avoid maxing out your credit limit. This demonstrates that you are a responsible borrower and may result in lower PMI premiums.

However, if your credit score is lower, lenders may view you as a higher risk borrower and charge higher PMI premiums. It’s important to maintain a solid credit history to increase your chances of being approved for a loan and receiving favorable terms.

Type of Loan

The type of loan you choose can impact the amount of private mortgage insurance (PMI) you’ll have to pay.

Fixed-rate loans offer less risk because the interest rate remains the same, resulting in consistent mortgage payments. This lower risk can lead to a lower PMI rate, potentially reducing the amount you need to pay.

On the other hand, adjustable-rate mortgages (ARMs) can bring more risk because the interest rate can fluctuate based on the market, making it harder to predict future mortgage payments. This could result in a higher PMI rate.

However, ARMs often have lower initial interest rates, allowing you to pay more toward your principal and build equity faster, potentially reducing the amount of PMI you need to pay.

Your lender can guide you through different loan options and help you determine how much PMI you should expect to pay.

How to Avoid Borrower Paid-PMI?

If you’re a home buyer looking to avoid paying borrower-paid PMI (BPMI), there are a few strategies you can consider.

One option is to make a larger down payment, as PMI is typically required for loans with a down payment of less than 20%.

Another option is to look into lender-paid PMI (LPMI), where the lender pays the PMI premium but may charge a slightly higher interest rate.

Finally, you could consider a piggyback loan, where you take out a second loan to cover the down payment and avoid PMI altogether.

1. Make a Large Down Payment

If you’re looking to avoid paying Borrower-Paid Mortgage Insurance (BPMI) on your home, consider making a large down payment of at least 20%. This will not only help you avoid BPMI altogether, but it will also give you more equity in your home from the start. Alternatively, if you already have BPMI and have reached 20% equity in your home, you can request to have it removed. And once you reach 22% equity, BPMI is often removed automatically.

2. Apply for FHA & USDA Loan

If you’re looking to avoid private mortgage insurance (PMI), you may want to consider taking out an FHA or USDA loan.

However, it’s important to note that these loans come with their own form of mortgage insurance. For FHA loans, this is known as mortgage insurance premiums (MIP), and for USDA loans, it’s guarantee fees. These fees typically last for the life of the loan, unless you have an FHA loan with a down payment or equity of 10% or more, in which case you’ll only pay MIP for 11 years. Ultimately, these fees will be in place until you pay off the house, sell it, or refinance.

3. VA Loan can help you

If you’re a veteran or active-duty service member looking to buy a home, taking out a VA loan may be a great option for you. Unlike other loans, VA loans don’t require mortgage insurance. Instead, they have a one-time funding fee that can be paid at closing or added to the loan amount.

The size of the funding fee depends on factors such as your down payment or equity and whether it’s your first or subsequent use of the loan. It can range from 1.25% to 3.3% of the loan amount.

However, if you’re a qualified surviving spouse or receive VA disability, you may be exempt from paying the funding fee. Additionally, if you’re refinancing with a VA Streamline loan, the funding fee is always 0.5%.

4. Piggyback Loan

If you’re looking to avoid paying private mortgage insurance (PMI) on a conventional loan, a piggyback loan may be an option to consider. With this approach, you make a down payment of at least 10% and take out a second mortgage, such as a home equity loan or line of credit, to cover the remaining amount needed to reach 20% equity on your primary loan.

If you take a second mortgage, you will have to pay it back with a higher interest rate. This is because if you can’t pay back your loans, your first mortgage will be paid first. Make sure to check if this will save you money or if it’s better to just pay the PMI.

How to Avoid Lender Paid PMI

If you’re looking to avoid lender-paid private mortgage insurance (LPMI), there are a few options available.

One option is to pay your entire PMI upfront at closing, which won’t require a higher interest rate. However, keep in mind that with LPMI, your payments are made as a lump sum upfront, so it’s impossible to cancel it.

Another option is to go with borrower-paid PMI (BPMI), which may be cheaper depending on the mortgage insurance rates at the time. With BPMI, you’ll pay a monthly premium until you reach at least 20% equity. While you can’t completely avoid paying for PMI with less than a 20% down payment, these options can help you save money in the long run.

The Pros and Cons of Private Mortgage Insurance

To begin with, there are both advantages and disadvantages of PMIs. Although, it can make it easier for you to qualify for a loan. PMI lowers the risk you present to the lender. A PMI gives you more buying power as it lowers the down payment that you are required to make every time. It can also act as an aid when you’re short of funds.

A primary drawback of PMI is that it increases the monthly mortgage payments and sometimes the closing costs too. Furthermore, PMI payments are no longer tax deductible. Although, you may be able to write off premiums on a loan taken out before 2017 (based on your income and the terms of the mortgage). Additionally, mortgage insurance has one more downside. It only protects the lender in case you default. It absolutely offers no protection to you (the borrower) if you lag behind in repayments.

1. Pros of PMI

- It enables you to qualify for a mortgage loan

- Allows you to make a smaller down payment

2. Cons of PMI

- It may increase the monthly payments

- Can increase the closing costs

- It provides no protection to the borrower

- The premiums are not tax-deductible

Reasons for Cancelling PMI (If you already have it)

There are several reasons why you may want to cancel your private mortgage insurance (PMI) if you already have it.

- One reason is if you have reached 20% equity in your home, regardless of whether you made extra payments towards your principal.

- Another reason is if you have made significant improvements to your home that have substantially increased its value. If your loan is owned by Fannie Mae, you must have 25% equity or more, while the Freddie Mac requirement is still 20%.

- You can also request removal of your mortgage insurance based on natural increases in your property value due to market conditions. But Fannie Mae and Freddie Mac require you to have 25% equity if the request is made 2-5 years after you close on your loan.

- After 5 years, you only need to have 20% equity. However, you must be current on your mortgage payments. For this, an appraisal must be done to verify property value for your request to be honored.

If you have a single-unit primary property or second home and don’t request cancellation. PMI is automatically canceled when you reach 22% equity. This is based on the original loan amortization schedule, assuming you’re current on your loan payments.

Canceling PMI On A Multi-Unit Property

The rules for canceling PMI on a property with many units are different. It depends on if you live there or if it’s an investment. For Fannie Mae loans, you can ask to cancel PMI when you have 30% equity. For Freddie Mac, you need 35% equity.

If you have a property with many units or an investment property with Freddie Mac, you need to ask to cancel the mortgage insurance. It won’t cancel by itself. But with Fannie Mae, the mortgage insurance cancels by itself halfway through the loan term.

Is There A Need to Pay for Private Mortgage Insurance?

A PMI typically costs around 0.5% -1% of your loan value on an annual basis. Although, it is subject to vary. The lender will look at your PMI premiums in detail on your initial loan estimate inclusively of the final closing disclosure form. Here, you choose to pay the premium upfront while closing or as a part of your monthly payments.

Bottom Line

Now that you know everything about private mortgage insurance you may pick and choose wisely. If you think you’re running out of time and can’t make outstanding mortgage payments. It’s probably time to sell your house fast for cash. Elite Properties can help you sell your house as we are a cash buying company and we assure to make the home selling process easy for you. For further information call us at 718-977-5462 and we will guide you through the selling process.

The biggest perk of being a homeowner is you can build home equity over the period of repayment. As you pay the mortgage your equity in a home increases simultaneously. Additionally, a Home Equity Line Of Credit (HELOC) is a financial product enabling homeowners to borrow a chunk of that equity against their homes. If you are someone who is thinking of using HELOC apart from securing a second mortgage loan; read our blog about why avoid using your home equity line of credit. And make a decision later.

What Is Home Equity?

Home equity or also known as real property value is the unencumbered interest of a property. It is the difference between your home’s worth and the outstanding balance of all credits on the property.

Example – Your home’s worth is $300,000 and you’ve paid $25,000 of the mortgage. Additionally, you’ve put down 20% ($60,000) which signifies you have $85000 equity in the home.

What Is A Home Equity Line Of Credit?

A HELOC (Home Equity Line Of Credit) is similar to a credit card. Although the limit is purely based on the equity you have in your home, most banks offer about 80% of your equity. HELOCs often have a lower interest rate in comparison to other loans and the interest may be tax-deductible.

As HELOCs have a lot to offer, using them for leisure and entertainment can be an indicator that you are misusing the allowance. Even if the HELOC is cheaper than a credit card, it is still a debt that must be avoided for funding a luxurious lifestyle. Given are some of the activities you must avoid while using your home equity line of credit.

Paying For A Vacation

Adding to other activities, spending your home equity line of credit on a vacation can be a bad decision. HELOCs are a source of cheaper debt in comparison to other kinds of credits, people use them for sponsoring trips. Also, the HELOC offers interest rates below 6% whereas credit cards may be on the steeper end offering 14%-25% interest rates. When you borrow from the home equity you are only aggravating the issue, as you may be risking your home while using HELOCs.

Buying A Car

There was a time where HELOC rates were reasonably cheaper than auto loans. Eventually, the cheaper rates enticed people, enabling them to use HELOCs although it’s not the case anymore. Furthermore, buying a vehicle or car, in this case, is a bad idea for many reasons. When you take an auto loan with a HELOC your loan is secured by the car you purchased. If your financial condition worsens you may end up losing the car. Additionally, if you’re unable to make repayments you may also lose your house. Adding to the rest, an automobile is a depreciating asset.

Paying Off Credit Card Debt

When calculating your repayments paying off expensive debt with cheaper debt may make a lot of sense. However, in some cases, this debt transfer can skip the underlying issue, which is a lack/shortage of income or inadequacy to control spending. It is vital to understand what led you to create credit card debt in the first place. You can only pay a credit card debt if you have the discipline to pay the principal of the loan initially.

Paying For College Education

The primary reason for people using HELOCs as mentioned above is because it’s cheaper than other credits. This makes it a big reason for using it for your child’s college education, however, using HELOCs may put your house at risk. You may have to think twice before using the home equity line of credit as it may risk losing your house. Additionally, if the amount is significant and you’re unable to pay the principal within 10 years. You may carry the added burden of mortgage debt into retirement.

Investing In Real Estate

Should I invest in real estate with HELOCs? The ultimate answer to this question is that it’s a risky proposition. There are many uncertain circumstances that may affect this decision. Reasons like sudden renovation, or a downturn in the real estate market, etc. can be a pitfall. Due to the same reason, many people have been trapped in debt, which makes repaying a tough task.

Bottom Line

There are many other ways to fund your requisites apart from HELOCs may it be for education, getting a car, or planning a trip. It is best to avoid using the home equity line of credit and use your savings or other available credit options. Furthermore, if you want to sell your house fast you can get in touch with Elite Properties. We are a cash buying company offering fast closings and no-obligation offers. Call us today at 718-977-5462 to know more.