The tax implications of selling a house vary depending on different circumstances such as your income level, type of capital gain, and so on. In some cases, they are minimal, while in others, they could be significant.

If you are planning to sell your house or have already done so, knowing the rules and provisions of these tax implications is crucial.

Selling your home is a big decision that can have a long-term impact. Ideally, before you put your home on the market, it’s important to know all the tax implications involved.

Your home is considered a capital asset and any net profit gained after selling the asset is assessed as capital gain hence, capital gains are subject to taxes. However, you may also get an exemption up to a specific limit under the IRS rules in certain circumstances.

Let us dive deep into the following guide about the main tax consequences of selling a home. By understanding these tax implications, you’ll be able to make an informed decision.

So, keep reading!

What Are Capital Gains Taxes?

As mentioned above in brief, capital gain taxes are the taxes imposed on capital gains. In other words, a capital gains tax is the tax that you pay on the net profit gained after selling your capital asset.

Securities, such as stocks and bonds, as well as tangible assets, such as real estate, vehicles, and boats, are subject to capital gains taxes.

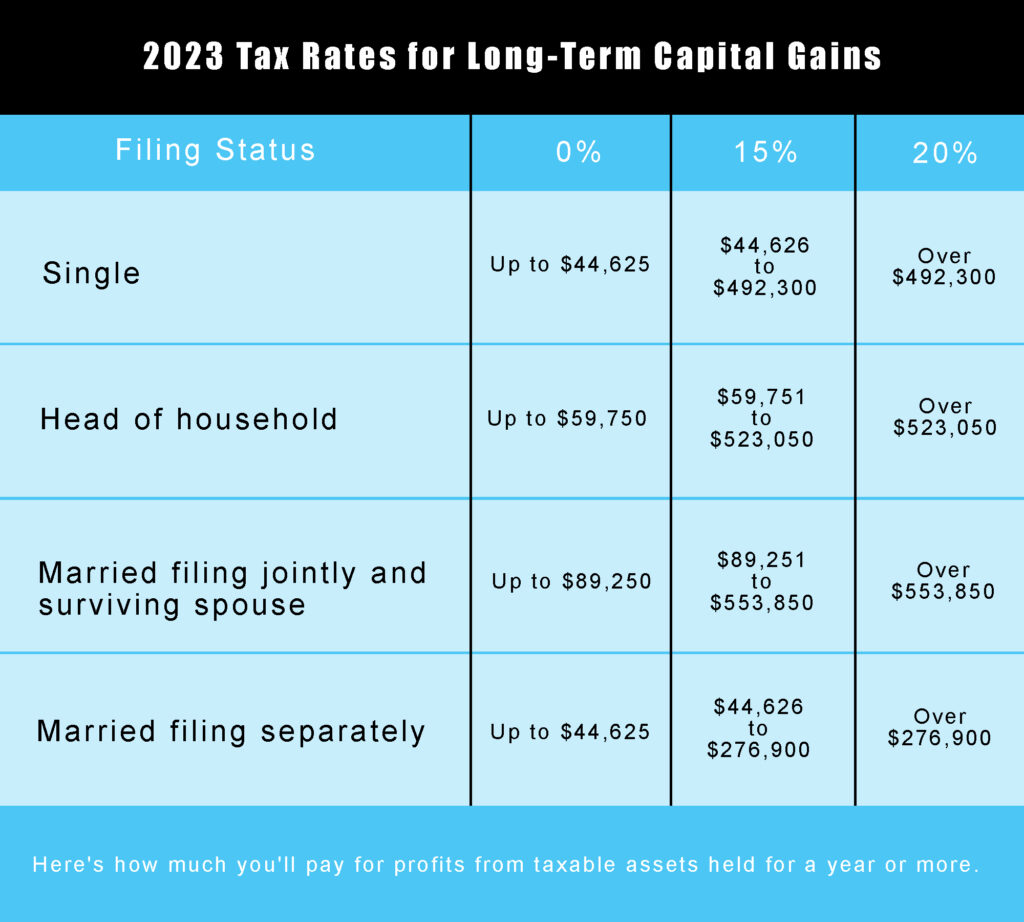

Here’s how much you’ll pay for profits from taxable assets held for a year or more.

The difference between the price you paid for an asset (your cost basis) and the price you receive when selling it (your selling price) is subject to capital gains tax by the IRS and many states.

How Does Capital Gains Tax Work?

Capital gains tax mainly depends on two main factors – your income level and how long have you owned your home. Considering these factors, you need to understand the two main categories that the IRS has divided capital gains into. These are:

1. Short-term Capital Gain – The profit that is realized from the sale of a capital asset that is held for a year or less is what we call short-term capital gain.

2. Long-Term Capital Gain – The profit that is realized from the sale of a capital asset that is held for more than a year is known as a long-term capital gain.

If you own your house for less than one year, the capital gain that you receive is consider as a short-term capital gain. Whereas, if you have owned the house for more than a year, it will be a long-term capital gain.

As a result, your tax implications will majorly depend on these circumstances and your income.

How Much Is The Tax?

You will be subject to taxation at your standard tax rate if you have a short-term gain. With preferential tax treatment, long-term capital gains are on tax at a rate of 0%, 15%, 20%, or 28%.

However, your income and tax filing status affect these rates.

According to IRS.gov, if your taxable income is less than or equal to $40,400 for single filers, $80,800 for married couples filing jointly, or qualifying widow(er), then some or all of your net capital gains may be subject to 0% tax.

How To Avoid Capital Gains Tax On The Sale Of Your House?

Homeowners are also eligible for a write-off from the IRS, which allows single filers to exclude up to $250,000 of profits and married couples filing jointly to deduct up to $500,000.

You are require to pay capital gains tax on the excess gain if you sell your house for a net profit exceeding $500,000 (for couples filing jointly) or $250,000 (for singles).

For instance, capital gain would be $800,000 if you and your spouse purchased your home for a cost basis of $200,000 and sold it for $1,000,000 many years later.

If you qualify for the specified exclusion, then $500,000 of this would be tax-free, but the remaining $300,000 would be a taxable capital gain.

To qualify:

- You must have owned the property for at least two of the previous five years.

- You must have lived in it as your primary residence for at least two of those five years to be eligible. The ownership and residence requirements do not have to be met simultaneously in the same two years.

- Additionally, you cannot have used the exclusion on a different house within the two years before the sale.

When Is The Capital Gains Tax Due?

You need not need to pay the capital gains tax until you sell your property. You owe any capital gains taxes for the sale of your house at the tax deadline associated with the year the sale closes.

The IRS recommends following their guidelines on this matter because there are several situations that may require you to make estimated tax payments.

Want to avoid writing a sizable check at tax time? Hence, it could be a good idea to report your estimated capital gains tax to the IRS as soon as the sales transaction closes.

The Final Say

When you sell your house, it’s important to be aware of all the tax implications of selling a house. The amount of tax you pay depends on various factors such as the value of the property, your income level, the period for which you are holding your property, and so on.

To reduce your tax burden, do your research to lay out all of your tax options and make sure that you are fully aware of your obligations.

As a last note, it’s important to emphasize that capital gains taxes can be a tricky subject with a lot of grey areas. It’s crucial to seek advice from an expert, licensed tax professional, specifically one who specializes in real estate matters. For more questions on Tax Implications Of Selling A House you can contact us.

Looking for more profound guidance? Get in touch today with Elite Properties!

Selling your vacation home can be exciting and challenging too!

Well, if you know the right process, you are good to go.

Your vacation home could be your second home. If you are planning to sell your vacation home, you must first need to understand that selling a vacation home is different from selling a primary home where you usually reside.

Understanding this difference in the first place is how you can get started with proceeding to sell your vacation home.

Let’s take a deep dive into this difference and how you can sell your vacation home effectively. So, keep reading!

Understanding the Key Differences Between Selling a Vacation Home and a Primary Residence

The place where you live the majority of the time during the year is your primary home. This period could be six or more months per year.

- Your primary residence is a place that provides more convenience to you such as it could be near your location of employment. Usually, the address of your primary residence is also listed on your important documents such as your driving license.

- A second home or recreational residence could be your vacation home. It is generally situated elsewhere than the owner’s primary home. Vacation homes are typically only used during certain times of the year.

The IRS classifies a second home as a “personal capital asset,” unlike your primary home, which is normally exempt from capital gains taxes (with a few exceptions).

Hence, you are required to pay capital gains tax after you sell your vacation home and abide by IRS rules when you file your taxes for the year you sell your second property or vacation home.

In addition to tax implication differences, there are also many other differences in selling vacation homes and primary homes. Also, vacation home homeowners are more dependent on real estate agents for selling than the homeowners of primary homes.

How Can You Sell Your Vacation Home?

Before you sell your vacation home, you need to ensure that you are ready with the prerequisites with other steps. So, here we go!

Prerequisites

- Selling a vacation home can be a daunting task, but with the right preparation and strategy, it can be a rewarding experience. Before listing your vacation home, it’s important to get an accurate estimate of its value. You can use home inspection services, or a real estate agent. You can also use online tools to get an idea of the home’s market value.

- It’s also important to have all the necessary paperwork ready, like title documents, repair estimates, and marketing materials. Once you have a good idea of the home’s value, it’s time to get it in shape.

- Make minor repairs and clean up the clutter. Finally, target potential vacation home buyers who are interested specifically in vacation properties.

All this will increase your chances of selling your vacation home quickly!

Researching Your Market

- There’s no question that vacation home selling can be a lucrative endeavor. But it’s important to do your research first. This includes understanding the market conditions and what properties are currently for sale.

- You can also interview the real estate agents in the area where your vacation home is to get an idea of the real estate market.

- Lastly, you also need to do research about the pricing and ensure to determine the fair market value of your vacation home.

Preparing The Vacation Home for Sale

- When it comes to selling your vacation home, preparation is key. Make sure to clean it and make any necessary repairs before listing it. This will give buyers a good first impression of the property and set the tone for what they can expect.

- Next, make some changes to the decor that will appeal to buyers. This can help sell your home faster.

- Finally, keep buyers informed about any changes or updates that happen throughout the home sale process. And we go! By making these enhancements, you’ll be well on your way to a smooth sale!

Marketing For Selling Your Vacation Home

- After you have a general idea of pricing and the market, and after your home is ready to be sold, start marketing your vacation home.

- There are a few different ways to market your home, and it all depends on what you’re looking for. Some popular choices include online listings, contacting local agents, or visiting homes in person.

- Make sure you have all the necessary paperwork ready, including an updated copy of your property tax statement and, as mentioned above, accurate information about any renovations or updates made to the home since purchase.

Listing Your Vacation Home

- Listing your vacation home for sale can be a demanding but gratifying experience.

- Before you get started, make sure you have a realistic idea of its market value. This will help you set a fair price for your home.

- Once you list your home, maintain a marketing campaign throughout the process and be ready to handle any inquiries or offers that come in.

Negotiating And Closing the Sale

- Once you start interacting with your potential buyers, you need to make sure that you are acing the game with great negotiation skills.

- The goal of negotiating and closing the sale of your vacation home needs to be to reach a mutually beneficial agreement.

- Correctly price your home and be ready to answer any questions a potential buyer may have to help them feel confident about making an offer.

- Before you put your home on the market, make sure all the paperwork is completed and ready to go to speed up the process.

Bottom Line

Selling a vacation home can be a smooth process if done right.

By following the above steps, you’ll be on your way to a thriving sale. Additionally, ensure to consider some essential details before listing your home for sale, especially the tax consequences of selling a vacation home.

Need more expert advice? Reach out to Elite Properties today!

In real estate, Cash Offer in Real Estate are often a go-to-choice, whether the buyer wants to compete with other buyers or take fewer financial risks, the seller wants to sell quickly, or both parties want to simplify the transaction.

As a result, it are often the best option, especially for buyers in certain circumstances. Buyers do not need a mortgage or any other financing when proposing a cash offer because they are not required to take on any financial risks.

To understand more about what a cash offer is, whether making a cash offer is a good idea or not, and what you need to do to make one, read on!

What Is a Cash Offer?

A cash offer in real estate means that a buyer offers to purchase a property where he or she is not using financing to pay the price of the property. This helps to bypass many time-consuming and expensive stages in the process that might make the house stay on the market longer than a seller would want.

In simple words, when a buyer can buy a house outright without taking out a mortgage loan, it is what we call a cash offer in real estate. Sellers usually prefer all-cash offers because they frequently close more quickly and have fewer risks than mortgage-contingent offers, which can experience delays and rejections.

Who Makes a Cash Offer?

A buyer is one who can make a offer to buy in cash in real estate. Particularly, this is a traditional buyer who has ready cash in hand or liquid assets to buy the house. It could also be a case where the buyer would have sold his or her previous property and kept the proceeds to avoid taking out a mortgage on their new property.

How is it Beneficial to Buyers?

There are many reasons why making a cash offer for a real estate property can be a wise decision for a buyer.

You can beat your competitor buyers and convince the seller to accept your offer by making a offer, which is usually accepted more quickly than other types of offers. Assure the seller that their property will sell as soon as possible.

For a buyer, one of the benefits of giving a cash offer is that it allows you to negotiate with the seller directly. Plus, another advantage is that closing the deal is usually easier if you’re able to come up with the full amount right away.

So, if you’re looking to buy a house while taking advantage of the latest market conditions along with an easy process, consider making a cash offer!

How Is Cash Offer Beneficial to Sellers?

Having cash offers makes the entire selling process quicker and smoother for sellers. Cash offers can delight the sellers mainly because of two reasons, the parties would close the deal sooner and the other that there is less risk.

The average time it takes to close on a standard sale is 49 to 56 days. It can be significantly shortened through cash offer sales involving direct purchasers.

Offer the seller the entire amount of the property without any mortgage loan or other financing. It becomes tempting for the seller with a quick sale and fewer closing expenses. The risk factor for the seller is low regarding the failure of the deal, as the buyer need not require appraisal and mortgage underwriting.

How To Make a Cash Offer?

Purchasing and selling homes with a cash offer differs from those with a mortgage. Here, the seller receives the offer from the buyer where the buyer may offer to purchase the property with a cheque or electronic transfer of funds.

However, as a buyer apart from the cash offer, and purchasing price you also need to prepare to incur expenses like property tax, insurance, and moving expenses.

Apart from all this, a seller may simply not accept the cash offer and as a buyer, you may require to show documentation and proof that you can pay the cash amount.

Once the seller accepts your offer, you’ll need to come up with an agreement on terms and conditions. Make sure to consult with an experienced real estate agent before making a cash offer – they can help you prepare the paperwork and ensure everything goes smoothly in the process!

Lastly, also remember that you would pay a big cash amount for the home price. Ensure the property is free from any problems by investing in a home inspection if your cash offer is going to accept.

Weighing the Advantages and Disadvantages

To sum up, here are some pros and cons of of it in real estate that you can consider.

Pros

- Quicker closing for both parties.

- Lower closing expenses are incurred.

- Interest charges on the mortgage is saved.

- As a seller, you may end up selling your property quickly.

- As a buyer, you can have better-negotiating power.

Cons

- The possibility of lower selling price due to lack of competition in buying the property.

- Great loss of liquidity on the buyer’s end.

- Without a mortgage, buyers lose out on certain interest or tax deductions.

- Investor buyers may unnecessarily bid up the price.

- A lack of trust may disrupt the whole transaction.

The Final Thoughts

A cash offer is a great way to ease up the buying and selling power in real estate. However, you also need to consider individually how beneficial it is to you as a buyer or seller.

Apart from this, you should also ensure to properly analyze the pros and cons of getting into a this transaction. Lastly, it is not too overstate that you need to do in-depth research before taking a decision.

Alternatively, you may also consult a real estate agent or real estate solutions companies. Looking for more expert guidance? Get in touch with Elite Properties today!

Increasing the value of your home can get you a great deal! But what is the heavy lifting that you are required to do to increase this value?

Regardless of whether you plan to sell it or renovate it, making appropriate improvements can increase the value of your home. Especially when selling your home, it’s essential to ensure that the value of your home is as high as possible.

There are several factors that impact the value of homes such as the location of your property, the age, size, space, and condition of the house, market conditions and the list go on. However, irrespective of these factors you can still increase your home value by making new improvements and upgrades to it.

Wondering where to start? We have got your back!

Let’s jump into the 5 best ways that can help you raise your home value.

Repaint Your Home

Home improvement or renovation can be a daunting task, but it’s definitely worth it to increase the value of your home. One of the best ways to do this is by repainting the home.

There are many types of paints and stains available that will perfectly match your home’s décor. It’s a smart investment to have a painter come out and paint your house – you’ll surely see a noticeable improvement.

If you’re looking to spruce up any dull areas, try adding new trim or curtains to bring a little color to your home.

Repainting your home is a great way to upgrade it without spending a fortune – and the best part is it is comparatively easier than other major home improvement options.

Add New Features to Your Home

One of the best ways to increase the value of your home is to add new appealing features.

There are many different options available, so it’s important to find the right one for you considering your spending budget and the condition of your home. Some popular features include porches, in-ground pools, and gazebos.

Other trendy options are to add smart features such as fire detectors, smart lighting, carbon monoxide detectors, smart doorbells, door locks, and smart speakers.

It’s important to consult with an expert before making any such decisions, as the right feature for your home can make a real difference.

Adding an attractive feature to your home is yet another effective way to see the home value jump up!

Update Your Home Flooring

Updating the home flooring is a common yet compelling improvement that homeowners make, but it’s often overlooked.

Having suitable flooring for the home is important for its look and feel, so ensure it is updated at the right time whenever required. Be sure to select the type that fits your needs and budget from the available options.

We have listed a few quick tips for updating your flooring to productively increase your home value:

- Add new carpet to the area wherever required.

- Change out the door mats or stair runner with trendy ones.

- Update your blinds and curtains that suit best with your décor.

- Last but not least, share good pictures of your renovations on social media!

Eliminate Unused Furniture

When it comes to making improvements to your home, there’s no better way to add value than by getting rid of unwanted furniture.

By freeing up space and making room for new captivating items and useful furniture, you’ll see your home’s value rising significantly in no time.

Not to mention, selling your unwanted items online or through a consignment shop can be a great way to make some quick cash. And of course, don’t forget to keep your eyes open to garage sales and estate sales to score the best deals on furniture!

Install New Lighting

One of the simplest and most cost-effective ways to do home improvements is by replacing old lighting with stunning yet energy-efficient options.

Various types of lights are available, so you can find one that fits your style and home. Additionally, installing light fixtures in strategic locations can help boost the aesthetics of your home.

Get creative and experiment with different types of light to make your home look its best!

You Can Also Read: 5 Reasons That May Reduce The Value Of A House

How To Improve Home Without Spending Much?

There are many ways to update the look of your home without having to spend extensively. Here are a few fantastic ideas that you can consider:

– You can change the décor and furniture under your budget. This can involve updating the paint colors, buying new pieces of furniture, or swapping out old pieces of furniture for newer versions.

– You can upgrade to hardwood, laminate, tile, or cork floors.

– You can also update the wallpaper, accessories, and other décors.

– Purchase new paintings, throw pillows, or lamps to add a more modern or stylish look to your home.

– Install smart thermostats, LED lighting, and other home appliances. This can help you save energy and improve the efficiency of your home overall.

Bottom Line

Enhancing your home effectively is crucially essential to increase its value. You can implement the most convenient yet appropriate options from the above-mentioned suggestions to raise your home value.

To sum up,

- You may start by painting your exterior and interior walls with a fresh coat of paint, this will instantly add value to your home.

- Next, you may upgrade any unfinished or non-functional features of your home – such as adding a new bathroom, kitchen, or deck.

- Further, you may update the flooring in your home to give it a fresh look and feel.

- Lastly, eliminate and replace unwanted furniture and add new compelling lighting to give a delightful look to your home.

These simple steps will help you raise the value of your home effectively and you’ll be able to upgrade your home without having to spend a fortune.

Looking for more expert advice? Get in touch with Elite Properties today!

With different trends surfacing in the real estate industry, realtors use all kinds of ingenious strategies to gain more clients. Home buyer rebate is yet another effective approach to attract more business.

Home buyer rebates or commission rebates are not legal everywhere. However, in Washington D.C. and 42 out of 50 states in the US (as of May 2022), including New York, real estate agents or brokers are allowed to give commission rebates to their clients.

When buying a home, if you are working with a realtor who provides home buyer rebates, you end up getting a part of the agent’s commission as a refund. Meanwhile, this approach also helps the agent to secure more business because they offer a rebate.

Since home buyer rebates are negotiable, you might need to ask for the refund that you want. But before we jump into how you can negotiate the home buyer rebate, let’s take a look at some essential aspects related to it.

What Is a Home Buyer Rebate?

When a real estate agent refunds a part of their commission on a transaction to a buyer, it is what we call a home buyer rebate, commission rebate, or buyer’s rebate. This can result in you getting thousands of dollars returned when you purchase a home.

Usually, a buyer’s agent receives 3% as the commission. The home buyer rebate is a portion of this 3% commission of the buyer’s agent which the buyer gets at closing.

Some real estate companies or agents may provide a buyer’s rebate or cash back as an inherent perk of using their services.

Is A Home Buyer Rebate Taxable?

If you are wondering whether you have to pay tax for a home buyer rebate or not, you can take a breath of relief. Under the IRS (Internal Revenue Service) rules, real estate rebates are not considered income earned but are treated as a price adjustment.

Hence, these rebates are not taxable and this adds a benefit while buying a home from an agent who provides commission rebates.

How To Negotiate a Home Buyer Rebate?

As providing a home buyer rebate cuts off the commission received by the agents or brokers, many may refuse to provide it.

The housing market in the United States is at an all-time high, so any savings that buyers can make matter. Getting a home buyer rebate while buying a house can help you save thousands of dollars. So, it is worth negotiating and getting the best amount of rebate that you desire from the agent or broker.

There are usually two ways through which you can negotiate a home buyer rebate:

⦁ Negotiation On Your Own:

As real estate agents have to share a part of their commission with you when they give a commission rebate, many of them become reluctant to share it.

However, those who understand the essence of getting more business by benefiting their clients may readily agree to provide you with a buyer’s rebate. In case you have identified a realtor providing rebates, you can simply negotiate for the home buyer rebate that you want.

An agent may put much less interest and effort into it if you negotiate for a greater rebate. So, you need to ensure that you present an offer that the agent can willingly agree to accept.

The rule is simple – if you want something you need to offer something. You may ask the agent for the desired rebate by providing a favorable offer.

You may assure the agent that you’ll engage them largely for their expert advice and bargaining skills, and conduct a greater portion of your home search on your own.

Make sure that you also stick to the best practices for negotiating a home buyer rebate such as:

- Do thorough research so that you are prepared to put forward the best offer.

- You may ask interrogating questions and be a good listener.

- Keep your points very upfront and ask for want you want.

- Hold in mind to expect the best outcome by aiming high.

- Last, but not least, be ready to walk away if the terms are not up to your liking.

⦁ Negotiation Through a Service:

Another alternative is working with companies that provide services to negotiate real estate buyers’ rebates for you. These companies find realtors who provide home buyer rebates and compete for your business.

These companies would negotiate on your behalf and get you the best deal. You can save both time and effort by using this method instead of negotiating with the agent for the rebate on your own.

This approach is comparatively easier as you need not put much effort into negotiating the rebate. As a result, it helps you to ease your negotiating process. This’ll save thousands of dollars through your home buyer rebate.

Situations Favorable for Negotiating Home Buyer Rebate

You may have a higher chance of successfully negotiating for a home buyer rebate that you desire if:

- You use the same agent to sell and buy your property so they can get both commissions.

- You are dealing in a market where the demand is low and the number of buyers is less.

- Your agent will receive a hefty commission when you are buying a high-priced home.

- You are working with a real estate agent who is newer and less experienced. He may have trouble attracting new clients.

The Final Say

With a home buyer rebate, you may be able to save a lot of money. It is feasible to negotiate the rebate on your own, but it may be challenging and provide certain service-level concerns. Alternatively, you may negotiate it through a service if you do not want to do the heavy lifting in negotiation.

Don’t just choose the agent offering the largest rebate. But compare agents to locate the one that best suits your needs.

Get in touch with Elite Properties’ expert support here!

When it comes to dealing in real estate such as selling, buying, or transferring your home, you may encounter many technical real estate terms and jargon. You must know the difference between House Title vs Deed.

Sometimes, you may also develop ambiguity or misinterpretations while transferring, selling, or buying your real estate property due to these terminologies. That’s why it is crucially important that you know what they mean so that you have clarity in your mind about the transactions or dealings that you are making.

Such most frequently used real estate terms are ‘title’ and ‘deed’. Title and deed are terms that are often used interchangeably. However, both are different concepts.

Both deed and title are very closely connected to each other and are related to house ownership. As a result, it may cause a lot of uncertainty.

So, let’s dive deep into understanding what house title and house deed mean and how they differ.

What Is a House Title?

When you buy a real estate property, owning the title is a vital aspect of the process and is legally important while complex too at the same time.

Having a title to property implies that you have legal rights relating to the ownership of the property. In simple words, a house title isn’t any physical document. But in fact, it is a concept that stands for having legal rights under the property’s ownership.

Someone else might be able to claim that they are the rightful owner of your home and that the person who sold it to you lacked the authority to do so if you don’t have a clear title to your property.

This can lead to significant legal repercussions so you should steer clear of it at all costs.

What Is a House Deed?

A house deed is a physical written document that transfers the ownership of a property from one party to another. In other words, titles are transferred by using deeds.

There are different types of house deeds such as General Warranty Deeds, Special Warranty Deeds, and Quitclaim Deeds. They are all serving their purpose.

Usually, in the buying and selling process of a house, the buyer and seller are required to sign this house deed in order to transfer the ownership of the property.

The person who signs the deed for transferring the title of the property is called the grantor. Whereas the person taking possession of the ownership rights is called the grantee.

Now that you are clear about what title and deed mean, let’s jump on to understand more in detail about how they differ.

What Is the Difference Between House Title and Deed?

⦁ Concept

As discussed above, the title conveys the ownership of a property and the associated legal rights. While a deed is a physical written document and represents the transfer of the title of ownership from the grantor to the grantee.

To understand the difference in a more simplified way, a deed is an actual physical document while a title is a concept. Also, a deed is a written document that is recorded officially in an assessor’s office or courthouse.

Despite their differences, it is also crucial to understand that they cannot exist apart. They both form part of the whole transfer process of the house.

⦁ Objective

When you claim you own the property it means you have title to it and have the legal rights to use it. On the other hand, a deed is the legal proof of this title and is a document used for the transfer of this property.

In a nutshell, the objective of a deed is to prove the transfer of ownership from one party to another. While the purpose of the title is to represent the legal rights to own, use, and modify a property.

A deed serves as the owner’s legal claim to the property. On the other hand, the title identifies the legal owner of the property.

⦁ Process

Before initiating the transfer process of the real estate property, it is to examine whether the seller owns the title and can sell the property. It is also checked if there are any associated limitations on the property for sale.

This is known as a title search. To check if there are any liens or conflicting claims against the property, public records are reviewed under the process of the title search.

After checking the public records, the title examiner will conclude and create a title abstract. This title abstract will state whether the seller has ownership or not and if he can sell the property or not.

Once the seller receives the approval for a clear title, the seller can go ahead with the closing process of selling.

Further, when the deed is received, the seller can transfer the title and ownership of the house by signing it. Then the buyer signs, inheriting the title and paying off the previous mortgage loan (if any).

This is how during the closing process, the title and the deed come into play at different points.

The Final Say

A valid sale or transfer of property requires both a proper property deed and a proper title. Both are a part of the process and play a significant role at different points.

Both concepts differ and are related to the ownership of the property, despite often being used interchangeably. However, both title and deed are important to accomplish the process and hold tremendous legal importance.

Dealings in real estate become easier when you have extended support from professionals. Elite Properties, based in New York, aims to make the process of buying and selling more manageable.

Having handled the most competitive and personalized services in real estate ensures to maintain transparency. It also has provisioning information related to real estate buying and selling.

For expert support in buying and selling your property get in touch with us today!

Are you moving to a new home? Or simply wish to make profits from the property in which you have invested? You can then rent your home.

Well, if yes, we completely understand the debate you are having in your head about whether to rent or sell your home.

The choice for anyone depends on various factors such as financial situation, market conditions, costs, and so on. So, what would be the most appropriate decision for you?

Both renting and selling the home have their pros and cons. You need to figure out what suits best for you as per all the conditions and factors around you.

So, let’s understand some of these factors that will help you decide if you should rent your home instead of selling it or not.

When Should You Rent Your Home?

If you are looking to make some extra monthly income, renting your home is a go-to option. But you also need to ensure that after incurring the additional expenses and taxes, you are still making a profit.

Here are a few factors that may support your decision to rent your home.

You Are Temporarily Moving

If you are moving to a new home temporarily, you may later require to return to the place where you are currently residing.

The reason could be anything, a temporary job shift, or temporary shifting to a location for some specific purpose. Renting your home in such a scenario will give you relief. You’ll have a home to live in when you return.

Not only this but renting a home could be comparatively hassle-free and cheaper. It is easier than finding a new home when you return.

You Want To Invest The Rental Income

As renting your home will give you a regular income. If you are looking for some extra earnings by investing this income, renting could be better for you than selling your home.

You could try various methods of investing. It can be rental income such as fixed deposits for reaping interest, government schemes, and so on.

Alternatively, you could also use the rental income to pay the EMIs of your new home if you have purchased it on loan.

Your Cost Of Renting Is Low

You can gain money in both renting and selling. However, renting and selling both have some costs involved.

What majorly determines your decision of whether to rent or sell your home is the profit that you gain after incurring all these costs.

The costs of renting may include home repairs and maintenance, insurance, taxes, the cost of vacancies, and so on. If these costs are low for you and if you are able to make enough profits, then renting your home could be a good choice for you.

When Should You Sell Your Home?

If the above-mentioned factors are in your favor you should go for renting. If not, then below are some factors that will help you make more sense in selling your home.

You Need Cash To Pay For Buying A New Home

If you are moving to a new home and you require liquid cash for purchasing it, you could sell your current home and utilize the proceeds from the sale for buying your new home.

Also, you are not required to opt for any mortgage loan and undergo the long approval process if the equity of your current home is enough to buy a new home. As a result, it will help you to pay your new down payment.

In case, your current home is the only one you could rely on to pay for purchasing the new home. So, there is no point in thinking about renting your home.

You Aren’t Ready To Become A Landlord

Renting your home can help you generate a passive income, but becoming a landlord comes with a lot of responsibilities. You also need to be prepared to take the additional expenses such as home maintenance, repairs, taxes, and so on.

You are also responsible to find “good” tenants and take up the cost of vacancies if any.

You may also reach out to some property management company to look after all these things. But they would charge you a percentage of your rental income. This will cause a reduction in your profits.

If you aren’t ready to take up all these responsibilities and costs as a landlord, deciding to sell your home may sound good to you.

You Are Existing In A Seller’s Market

If you are in a seller’s market, where the number of buyers is more than the homes available for selling, then you should think about selling your home.

As the buyers in such a market have a limited number of options to select from. You can manage to get more attention to get your property sold.

You may also get an opportunity to increase the value of your property. You can also get genuine buyers that will pay the value that you desire.

If you think you will be able to incur the associated selling costs yet make enough profit by selling your property in such a market than the rental income that you could get, selling your home more would make more sense.

Final Thoughts

Deciding whether to rent or sell your home, requires you to analyze certain important factors as mentioned above such as costs, profits, responsibilities, market conditions, and so on.

It is also important for you to understand your goals and consider your financial situation and lifestyle choices while deciding whether to rent or sell your home.

In addition to conducting thorough research, you can also seek the opinion of a professional real estate agent or company. They may help you to make the most appropriate decision by providing you with information about the current real estate market conditions, the value of your home, or the rent charged in your area.

Get in touch for a more expert opinion!

Having a real estate broker by your side is exceedingly indispensable when trying to sell your home. You need several networks and the real estate market know-how to crack a good deal. You have to search for the Flat Fee Real Estate Broker.

However, it isn’t so favorable to pay hefty commissions to these real estate brokers to get your job done. Especially if the commission rates are too high.

Here’s where having a flat fee real estate broker can be your go-to strategy to sell your home. But how far is selling your home through a flat fee real estate broker beneficial for you?

Let’s try digging more into this.

How Does the Flat Fee Model of Real Estate Brokers Work?

When a real estate broker charges a fixed fee rather than a percentage of the sale, it’s a flat fee.

For instance, in a commission-based transaction, you may pay 5% as a commission on a sale amount of $200,000 to the broker. However, in a flat-fee transaction, you will pay a fixed amount for the above sale, which could be $3,500.

So basically, if you pay the broker a commission of 5% on the sale of $200,000 you would pay $10,000.

While, if you are paying a flat fee, you may pay the same amount which is $3,500 no matter if the house sells for $100,000 or $1,000,000.

Pros Of Using a Flat Fee Real Estate Broker

You can win a great deal for your home using a flat fee broker. Below are some pros of flat fee real estate brokers that you must consider.

1. Getting More Control:

At times having more control over the selling process can be advantageous for you. As a result, you could have the ability to make several decisions following your preferences and convenience.

By using a flat fee broker, you may get control over many important selling aspects such as deciding the home price, handling negotiations, or selecting options to market it.

You may also get control to decide if you want to have an open house and not be at the mercy of the broker’s schedule.

Not only this but with some flat fee brokers you may also get the authority to decide if you want to sell the home with the full support of an agent or with a limited one.

2. Saving More Money

As the flat fee charged by the broker does not depend upon the selling price, it can potentially be less and you may end up saving more money. In other words, you may save more of the proceeds from your final sale amount after paying a fixed fee.

In the above example, whether your sale amount is $100,000 or $1,000,000, you shall pay a fixed flat fee that is $3,500. If your sale amount is greater, you may save more under the flat fee model.

It is also observed that usually flat fees are lower than commissions. Hence, you may save money. However, it also depends on the terms that you agree upon with your broker.

3. Proper Budgeting:

Flat fees are mentioned in the listing agreement and usually do not vary as per the final sale amount of your home.

Hence, as a seller, this helps you to do proper budgeting to make things fall in place properly.

It’s especially helpful when your budget is tight. You know what fee exactly you will pay the broker and plan accordingly on your net proceeds.

If you are a seller who is tight on budget and prefers knowing promptly what you will have to pay the broker before your sale to avoid any kind of uncertainty, you should go for a flat fee real estate broker.

Cons Of Using a Flat Fee Real Estate Broker

Even if you may potentially pay less using a flat fee model, it has drawbacks too. Here’s what you need to consider.

1. Getting Limited Services:

Getting more while paying less is something very rare, as you usually get what you have paid for.

A flat fee broker may not provide all the services that he/she would have while working on a commission-based model.

You may get very limited services. The broker may also list your home only on the local MLS which is just not enough to get a good deal.

However, it is not bad to get a few services for paying less, but it still depends on your selling goals and the current situation that you might be in.

2. Earning Less Profit:

You may sacrifice your profit if you choose to use a flat fee real estate broker.

This is so because flat fee real estate brokers have less motivation (no incentive) to negotiate and get you the best deal with top dollar for your home.

Flat fee brokers usually consider volume to make it big and hence, they may not dedicate much time and effort to negotiating to increase your profit.

3. Paying for Additional Expenses:

You can save more money by paying a flat fee and not high commissions, but you may also have to incur some additional expenses.

You may require to spend on marketing, pricing, and other closing activities, which otherwise a commission-based agent would have done.

Your flat fee agreement may include only listing your home on MLS. For attracting more buyers, you are required to incur additional expenses. Hence, it is recommended to consider these expenses before you go for flat fee brokers.

Bottom Line

A flat fee model can help save money, but on the other hand, you also need to be ready to handle other activities associated with selling on your own.

So, depending on your goals you could thoroughly analyze both the pros and cons and decide as per your situation and objectives whether to go for a flat fee real estate broker or not.

For expert opinion contact Elite Properties today!

Pricing your home is the heavy lifting that you need to do when you make up your mind to sell it.

A home’s price is determined by several relatable factors that are unique and different in some way.

It could be that you are considering moving to another area or that you simply want to live in an upgraded house, but selling the existing house can be just as challenging as finding a new one.

There would have been many questions on your mind. This applies especially to the price of your home, such as whether to price according to market value or above or below it.

Figuring out the sale value of your property can be complex and tricky.

It could be difficult to decide what features of your home can help you get a higher value and what cannot. Additionally, how to do pricing concerning the market value of the house can also be tough.

However, if done right you are not far from cracking a good pricing deal for your home while selling.

So, let’s take a look at some expert suggestions and guidelines below on how you can determine an appropriate price for your home for sale.

How To Price Your Home Appropriately?

Use Online Home Value Estimator:

The internet is loaded with tools to estimate your home value for sale. Using an online home value estimator can be a good start for deciding the price of your home.

You need to enter certain details and answer a few questions. As a result of which, the online home value estimator shall provide you with an estimated range of valuation for your home.

It usually finds the available data such as the current value of your home by comparing your property and its features with some other similar listed properties that have a recent sales record.

Online home value estimators shall only provide you with a reasonable price. They do not give the exact data required to do proper pricing for your home. However, it can still help you to get a kickstart.

Connect With a Local Real Estate Agent:

An online home value estimator can just provide you with an approximate idea about the pricing of your home as these estimators use limited data.

Therefore, the next step that you need to take is to approach a well-experienced local real estate agent.

The agent may consider the factors that an online home value estimator may not, such as the recent advancements, the locality of your property, and local buyer opinions and beliefs in the region.

Not only this but the agent may also tend to have inner information about the ongoing sales of homes in your area. The agent can provide you with the best piece of advice on valuing your home at the fairest price.

Conduct Comparative Market Analysis (CMA):

As the housing market conditions change dynamically with time, it is important to stay updated and switch the recent updates and trends for pricing your home rightly.

Conducting a comparative market analysis (CMA) is one of the best ways to price your home for sale appropriately.

You could ask your real estate agent to do this analysis. He/she should review and compare the information about the most recently sold homes in your local market. These are called ‘comparables’ or ‘comps’.

In other words, comparables are homes that are similar to yours and are recently sold. They could be similar in terms of amenities, structure and size, location, and so on.

These comps can be a good consideration when pricing your home for sale.

Know Your Housing Market:

It is crucially important to understand the housing market you are in. The pricing strategy that you shall adopt will be greatly influenced by this.

Usually, there are three types of markets based on which you can decide the pricing of your home:

Seller’s Market:

In this market, the number of buyers is more than the number of homes for sale.

As a result, you can price your home slightly higher than the market value for your home, as the buyers here are contending for fewer homes.

Buyer’s Market:

In such a market, the number of homes to be sold is more than the number of buyers.

Hence, you are required to price your home slightly less than the market value for the house to attract buyers.

Neutral Market:

This type of market has a balance between the number of homes to be sold and the number of buyers for the same.

You need to make sure that you analyze your comparables and try to keep prices accordingly and compete to attract buyers.

Considerations When Setting Your Home’s Price:

While strategizing about the price of your home, you may fall for some common mistakes. That is why the below considerations should be viewed to specify the right price.

- Set aside your emotions to determine a realistic price for your home.

- Don’t overemphasize home improvements, as not all renovations and upgrades have higher ROI.

- Try to understand the buyer’s perspective while setting the price.

- Adjust the price or strategy as and when necessary.

To Sum Up

By applying the above guidelines for pricing your home, you are less likely to disappoint your potential buyers by quoting an overvalued price. You can be assured that you are not underselling your home.

Make sure that you are conducting a profound comparative market analysis and approaching a trusted real estate agent. The more data you collect, the higher the chances are that you will quote the right price for your home.

For more proficient recommendations, get in touch today!