If you want to buy a home with minimal hands-on effort or don’t want to do the heavy lifting to purchase it, buying a Turnkey Properties can be your go-to option. Probably you might have already researched and looked for easy options to buy a suitable property, and must have come across an option of turnkey if not, we have got you covered! Nevertheless, turnkey has both benefits and drawbacks, so it’s better to understand if buying a turnkey property is really a good option for you or not.

So, let’s dig in to know what turnkey property means in real estate, and its pros and cons for you as a buyer.

Here, we go!

What Is A Turnkey Property In Real Estate?

A turnkey property is ready for occupancy right away and doesn’t need any significant renovations or repairs to be livable.

In other words, turnkey refers to a property that has been completely renovated and doesn’t even require a new coat of paint in certain situations. Sometimes, it also means a fully furnished home. This can be a duplex, apartment building, or even a single-family house.

Purchasing a turnkey property generally entails working with a company that specializes in the restoration of older properties. To take care of the standard homeowner responsibilities for the property or home you own, some companies or real estate developers also provide property management services.

Pros Of Buying A Turnkey Properties

We have mentioned some of the essential pros of buying a turnkey property for you below. Let’s have a look!

- Renovation Isn’t Your Responsibility

Of course, the most significant advantage of buying a turnkey property is that it saves you the time, and effort that comes with renovations and day-to-day handling activities. If you wish to avoid doing renovations or Want to move in straight away, then a turnkey home could be the best option for you. - Facilitates Easy Renting

You won’t need to do a lot of work to rent out the turnkey home you buy. The restoration company takes care of everything, so you won’t have to paint, renovate, or fix anything before the house is ready for your tenants. - Quick And Strong Cash Flow

Due to the expense of making repairs and the time it takes to find qualified tenants. Usually rental properties may not turn a profit for a considerable amount of time. Investing in a property that is ready to move into reduces the amount of time it can take to get your first rental income. On the other hand, since some turnkey properties have just undergone renovations, repair expenditures can be minimal in the initial years. The first few years might see a strong cash flow from this. - Less Maintenance

Some businesses that offer turnkey homes will also take care of the property management. Property management companies will take care of many things, from collecting rent to handling upkeep. This means less effort and maintenance on your part.

Cons Of Buying A Turnkey Properties In Real Estate

Now that you know some of the vital pros of buying a turnkey property. You must also consider its cons so that you can make an informed decision.

- Less Control

Since the turnkey company chooses which properties to renew, you won’t have much say in the exact location of the property while buying. Further, with turnkey real estate investments, you might not have much influence over the tenants residing in your rental property or the upkeep and repair process. Although having less control means less effort. This means that your entire investment is in the hands of someone else, who is probably not going to be driven to ensure the property operates to its full potential. - Risk Of Poor Property Management

Selecting the right property manager is crucial. Since they will look after everything right from taking care of maintenance, to handling any other problems at your property. There’s always a risk that your property manager won’t perform well especially if you are unable to keep an eye on or visit the property frequently. This could cost you money as well as reduce your ROI. - You Might Pay Too Much

As turnkey properties are move-in ready and do not require any vast repairs or renovation, they are usually expensive. If you are renting your turnkey property, your monthly cash flow will be negatively impacted by the cost of paying the property management to maintain it. When you factor in all of those extra management and maintenance expenses. You might discover that you’re not earning nearly as much as you would have. If you had purchased, fixed, and cared for the home yourself. - Lack Of Personalization

As you get the house in a ready-to-move-in condition and the renovation is all taken care of by the turnkey company. You don’t get to intervene much in the upgrades and overall look and feel of the house. This leads to a lack of personalization on your part. For buyers who are imaginative and enjoy adding special touches to their property. Turnkeys don’t provide many possibilities because they won’t be involved in the renovation process.

The Final Say

Indeed, a turnkey property is a fantastic choice for both homebuyers and real estate investors. It eliminates a lot of the tedious steps involved in purchasing and upgrading a house.

Before moving forward, though, you should confirm that a turnkey property meets your requirements and objectives.

Purchasing a turn-key property will come at a higher cost. Even though you will save money and time on contractors and repairs. To make sure the house is genuinely worth the premium. It is recommended to engage an inspector and arrange for a viewing of the property first.

Want to seek an expert’s advice? Our team of professionals goes above and beyond to assist you with profound guidance. They will help you make informed decisions while dealing in real estate properties. Get in touch with Elite Properties now!

A revocable trust or living trust often becomes the preferred vehicle of choice for people who wish to disperse their worldly assets in a complex or specific manner.

This flexible instrument can offer them a plethora of advantages and safeguards. This is to guarantee that their financial requirements and preferences are efficiently satisfied both throughout their lifetime and after they pass away.

While setting up a revocable trust for real estate holding may be familiar to you. Also, you might be wondering, “How beneficial is it to sell a property held in such a trust?”

If you have researched a little bit, you might be aware that the process entails more than simply handing the property deed and receiving payment. Although selling a house held by a revocable trust can be complex. It can still streamline your property sale.

Let’s find out how and here we go!

Understanding Some Basics

Before diving deep into understanding how can a revocable trust streamline your property sale. let’s get clear with some basics.

What Is A Trust?

In a trust, assets are transferred from one person (the trust settlor/grantor) to another (the trustee), who is responsible for managing the assets. Anything from vehicles to bank accounts to valuables and real estate can be held under a trust.

The trustee manages the trust on behalf of the beneficiaries under the conditions set forth by the grantor.

What Is A Revocable Trust?

A revocable trust, (revocable living trust or RLT), is the most flexible type of trust that you can create. As long as you are competent, you can amend or revoke your trust with an RLT at any moment during your lifetime. For instance, you could sell trust property, add or remove beneficiaries, or transfer additional assets to your trust.

To enable themselves to use and manage their assets more effectively. While they are still living, many grantors choose themselves as the RLT’s original trustee. If you go this path, you should designate a successor trustee to oversee your trust if you pass away or become incapable of managing it yourself.

However, your RLT becomes irrevocable upon your death, which means it usually cannot be revoked or altered.

Usually avoiding probate is the main reason for putting assets in a revocable living trust. In the absence of a trust, your heirs may have to endure a protracted and stressful legal process to get their personal property through after your death.

Advantages Of Selling Property Held In A Revocable Trust (Before Death Of Grantor)

If you are the owner of a house in a revocable trust, selling it (as far as the legal aspects are concerned) is no issue. The trust can be altered or dissolved as you see fit. To make your choice, you have two options:

- If you hold the dual role of grantor and trustee, you have the option to sell as the trustee and retain the proceeds within the trust, or

- You can change the home’s title to your name and sell it personally, outside of the trust.

But just like with any other sale, you will have to pay capital gains taxes in both situations. But, if your circumstances allow it, you can also apply to have the capital gains tax excluded.

Advantages Of Selling Property Held In A Revocable Trust (After Death Of Grantor)

Putting your house in a revocable living trust will make it easier for your beneficiaries to sell it when you pass away.

If you didn’t have a revocable living trust, the sale of your property would involve all of your heirs equally. This implies that all decisions about the sale, including the following, would require consensus from all parties:

- They can sell a house or kept in the family.

- Whether or not to make improvements to the house to raise its worth before selling.

- Which real estate agent to work with?

- Listing price.

- What offers to accept?

Certain families might have no trouble making these choices. However, juggling these tasks appropriately while dealing with the stress and grief of losing a loved one is a challenge for a lot of family members.

The sole successor trustee under a revocable living trust can alternatively handle the property sale. By exercising their fiduciary duty, the trustee can decide on all of the aforementioned matters. Also, make sure that the sale is carried out in the beneficiaries’ best interests. Then, evenly divide the money from the sale among the heirs.

To Sum Up

From the above explanation, you can sum up the benefits of selling property under revocable trust as follows:

- You can bypass the traditional sales process, and save money on repairs, long delays, and other costs.

- Increased flexibility and control over the terms of the sale, enabling the negotiation of a desirable closing date and price.

- Beneficiaries can obtain inheritances quickly and effectively.

- The ability to allocate sale proceeds to beneficiaries’ needs and financial objectives.

- Possibility of lower tax obligations than with traditional sales.

- Privacy preservation in contrast to the public probate procedure.

- Asset protection for assets within the trust.

- Simplified procedure managed by the trustee acting in the beneficiaries’ best interests.

Whether you are the grantor or benefactor, selling a home takes time, even after resolving the legal considerations. To sell your house, you must perform the necessary improvements, stage open houses and showings, find the ideal buyer, and do other tasks. However, Elite Properties can help you sell swiftly and for top dollar.

Elite Properties maintains a reputation for transparent business practices and offers sincere guidance. Our vast network of skilled real estate agents has handled millions of dollars worth of real estate sales and purchases.

To meet your real estate needs, our team goes above and beyond the call of duty. We give our clients detailed information on how to manage various real estate matters, including real estate purchases and sales. Learn more about us.

To hold real estate transactions smoothly, a better understanding of the process and support from experts or professionals is required to solve you real estate FAQs. Whether you are buying a house or selling one, you may be flooded with tons of doubts and queries in your mind at every step.

Getting answers to all such queries and doubts by preparing and educating yourself on how things work helps to easily navigate your real estate transaction with the help of real estate FAQs. In this guide, we have listed and answered some of the most common real estate FAQs that can pop into your mind while buying or selling your home.

So, let’s dive deep into the Real Estate FAQs guide and make it easy for you!

Common Real Estate FAQs When Selling A House

1. What is a Seller’s market?

A seller’s market, there’s a scarcity of goods up for grabs, granting sellers the upper hand in setting prices. This term is often used in the real estate when there’s a low supply and eager buyers.

2. How long will it take to Sell My House, a most important Real Estate FAQs?

A house generally takes 55 to 70 days to sell. This comprises 25 days on market and a 30- to 45-day closing period. Research shows that, as of March 2023, on average, it can take 54 days to sell your home. However, the exact answer to how long will it take to sell your house ultimately depends on certain factors such as the condition of the house itself, the real estate market conditions in your area, the time of the year that you are listing, property location, and the asking price.

3. What are some Effective Pricing Strategies for Selling a home?

Pricing your home correctly is crucial to attract buyers and sell it within a reasonable timeframe. One effective strategy is to price your home competitively based on comparable properties in your area. Overpricing can deter potential buyers, while underpricing may result in leaving money on the table. Another strategy is to consider the current market conditions. If it’s a seller’s market with limited inventory, you may be able to set a higher asking price. However, in a buyer’s market with more competition, pricing slightly below market value can generate more interest and potentially lead to multiple offers.

4. How do I prepare my house before Selling?

Making your house presentable is the first step in getting ready to sell. This entails doing minor repairs and thoroughly cleaning the entire house. Help customers in ensuring the proper functioning of the HVAC, plumbing, and electrical systems. Every room should appear tidy, uncluttered, and free of obvious damage. Alternatively, you can also consider professional staging which can help buyers envision themselves living in the home

5. How to determine the Selling Price of my house?

The neighborhood and the asking price of comparable-sized homes are some of the most important factors to consider while determining a house’s selling price. Getting a thorough comparative market analysis from a local realtor is one of the best ways to determine whether you are selling your house for the proper price. Also, check the age and condition of your house which will affect the property value. Yet the market is important. Just like anything else, supply and demand affect how much a property costs.

6. What are the documents that the buyer will need from me?

The original Title Deed, Sale Deed, Encumbrance Certificate, and any relevant tax receipts could be requested by a buyer while selling your home.

7. How can I navigate the Negotiation Process when Selling My Home?

Negotiating the sale of your home can be a delicate process. It’s important to approach negotiations with a clear understanding of your priorities and be open to compromise. Work closely with your real estate agent to determine your bottom line and set realistic expectations. Consider factors such as the current market conditions, the buyer’s offer, and any contingencies. Your agent will help you negotiate the best possible terms and guide you through counteroffers and potential repairs requested by the buyer. Remember, the goal is to reach a mutually beneficial agreement that satisfies both parties.

8. Another Real Estate FAQs, What is the Commission Paid to an agent?

Instead of receiving a fixed fee, the seller generally pays the agent through a commission in a real estate transaction. The commission charge often amounts to 5–6% of the ultimate sale price of the house. The commission fee is usually split equally between the agents representing the seller and the buyer each taking home 2.5–3%.

9. Why does the Assessed Value of my house vary from its Market Value?

Your home’s market value can be more than its assessed value in a seller’s market. This is a result of low availability, which makes buyers willing to pay more than the house is technically worth. On the other hand in a buyer’s market, because there will be a lot of competition from other sellers, buyers may make an offer that is less than the home’s assessed value.

10. Should I consider a Fixer-Upper or a Move-In Ready Home?

The choice between a fixer-upper and a move-in ready home depends on your personal preferences, budget, and willingness to take on renovation projects. Fixer-uppers can offer great potential for customization and increased equity, but they require time, money, and effort to bring them up to your standards. Move-in ready homes, on the other hand, are ready for immediate occupancy but may have a higher price tag. Consider your renovation skills, availability of funds, and timeline when deciding which option is best for you.

Pricing Strategies For Selling a Home Real Estate FAQs

1. What is a Comparative Market Analysis, and how does it help determine the right listing price?

A comparative market analysis (CMA) is a tool used by real estate agents to determine the appropriate listing price for a home. It involves analyzing recent sales of similar properties in the area, taking into account factors such as location, size, condition, and amenities. The CMA provides valuable insights into the current market conditions and helps identify a price range that will attract potential buyers. By comparing your home to recently sold properties, you can ensure that your listing price is competitive and reflective of the market value.

2. What are the advantages of pricing slightly below market value?

Pricing your home slightly below market value can create a sense of urgency among buyers and generate more interest. It can lead to multiple offers and potentially result in a higher final sale price. Buyers often perceive homes priced below market value as a great deal and are more motivated to submit competitive offers. This strategy can also help your home stand out among the competition and attract a larger pool of potential buyers. However, it’s important to consult with your real estate agent to determine if this strategy is appropriate for your specific market and property.

3. How can I attract Potential Buyers in a competitive market?

In a competitive market, it’s essential to make your home stand out to attract potential buyers. Start by ensuring your home is in excellent condition and address any necessary repairs or updates. Consider offering incentives such as a home warranty, seller-paid closing costs, or a flexible closing timeline. Additionally, invest in professional staging and high-quality photography to make your listing visually appealing. Finally, work closely with your real estate agent to develop a comprehensive marketing plan that includes online listings, social media promotion, and targeted advertising. These strategies will help increase visibility and attract serious buyers.

4. What are Closing Costs?

Closing cost refer to additional charges beyond the property’s purchase price that both buyers and sellers need to cover to finalize a real estate deal. These expenses can comprise various fees such as loan initiation charges, property valuation fees, title examinations, title protection, land surveys, taxes, deed registration expenses, and fees for credit reports.

Expert Tips On Preparing a Home For Sale For Real Estate FAQs

1. How can Staging my home help sell it faster?

Staging your home can significantly impact how potential buyers perceive the space. It involves arranging furniture, adding decorative elements, and creating a welcoming atmosphere that showcases the home’s best features. Staging helps buyers envision themselves living in the space and can make a significant difference in how quickly your home sells. Professional staging companies can provide guidance on furniture placement, color schemes, and accessories that will appeal to a wide range of buyers. If hiring a professional stager is not an option, you can still make small improvements by decluttering, rearranging furniture, and adding fresh flowers or plants.

2. What are some Cost-Effective ways to increase curb appeal?

Curb appeal plays a vital role in attracting potential buyers to your home. Fortunately, there are several cost-effective ways to enhance the exterior of your property. Start by cleaning up the yard, mowing the lawn, and trimming overgrown bushes or trees. Add pops of color by planting flowers or placing potted plants near the entrance. Make sure the exterior of the home is clean and in good repair – consider power washing the siding, repainting the front door, and replacing outdated light fixtures. Lastly, don’t overlook the small details – ensure the house numbers are clearly visible, and the mailbox is in good condition.

3. Should I hire a Professional Photographer to showcase my home?

In today’s digital age, high-quality photographs are essential for attracting potential buyers online. Professional photographers have the skills and equipment to capture your home in the best possible light. They know how to showcase the home’s features, create inviting images, and make the space appear larger. Hiring a professional photographer is especially important if you have unique architectural elements, stunning views, or a well-designed interior. The investment in professional photography can significantly impact the number of showings and the speed at which your home sells.

Common Real Estate FAQs When Buying A House

1. What is a Buyer’s Market?

In a buyer’s market, purchasers hold the upper hand over sellers due to an abundance of supply compared to demand. Consequently, prices tend to remain depressed, offering buyers a plethora of choices while compelling sellers to maintain competitive pricing. This scenario grants buyers greater leverage in negotiations.

2. What are the first steps in the Home Buying Process?

The home buying process can feel overwhelming, but understanding the first steps can help ease your concerns. The first thing you should do is determine your budget and get pre-approved for a mortgage. This will give you a clear idea of how much you can afford to spend on a home. Next, start researching neighborhoods and make a list of your must-haves and deal-breakers. Once you’ve done your research, it’s time to find a real estate agent who can guide you through the rest of the process. They will help you find suitable properties, negotiate offers, and navigate the closing process.

3. How can I finance my Home Purchase?

Financing a home purchase is a crucial aspect of the home buying process. There are several financing options available, but the most common ones are conventional loans, FHA loans, and VA loans. Conventional loans are not backed by the government and typically require a higher credit score and down payment. FHA loans are insured by the Federal Housing Administration and are more accessible to buyers with lower credit scores and smaller down payments. VA loans are available to veterans and active-duty military personnel and often require no down payment. It’s essential to speak with a mortgage lender to determine which option is best for you.

4. What’s the average credit score I need to buy a home?

Most loan programs need a FICO score of 620+. Higher scores mean less risk for lenders, offering perks like lower down payments and better rates. On the contrary, lower scores might mean higher upfront amounts or interest rates to mitigate the lender’s perceived risk.

5. What factors should I consider when buying a home?

When buying a home, several factors should be taken into consideration. Location is one of the most critical factors. Consider the proximity to schools, work, amenities, and transportation. Safety is also crucial, so research crime rates and neighborhood statistics. Additionally, think about the size and layout of the home. Does it meet your current and future needs? Don’t forget to consider the condition of the property, including any necessary repairs or renovations. Lastly, evaluate the potential for appreciation and resale value. Taking these factors into account will help you make an informed decision.

6. Should I Sell My Current House to Buy a New One?

It mostly depends on your financial situation and capacity to locate temporary housing. It is advisable to sell your current house before buying a new one if you require additional equity to buy a new house or to satisfy a mortgage requirement. Having said that, you will probably require temporary housing or a short-term rental elsewhere.

7. What should I do when I want to Buy a House?

Getting a mortgage approved is the first and foremost stage in the home-buying process. Buying a new house will be extremely difficult without a mortgage approval. Most people don’t have sufficient funds to buy a house altogether. Therefore, a mortgage functions as a safe loan that has a fixed interest rate.

8. Am I required to do a Home Inspection?

An expert inspector can provide feedback on any local code concerns as well as structural and aesthetic concerns. A house inspector will also assist you in valuing the house more accurately.

9. How does the Home Inspection Process work?

The home inspection is a crucial step in the home buying process. It involves hiring a professional home inspector to assess the condition of the property. The inspector will examine the home’s structure, systems, and components, including the roof, foundation, electrical, plumbing, and HVAC systems. They will identify any potential issues or defects that could affect the property’s value or safety. After the inspection, you will receive a detailed report outlining the inspector’s findings. This report will help you make an informed decision about whether to proceed with the purchase, negotiate repairs, or request a credit from the seller.

10. What are some common red flags to look for during a home inspection?

During a home inspection, there are several red flags that buyers should be aware of. Some common issues include water damage, mold, structural problems, faulty electrical wiring, plumbing leaks, and signs of pest infestation. These issues can be costly to repair and may indicate more significant problems with the property. It’s important to carefully review the home inspection report and discuss any concerns with your real estate agent. They can help you determine if the issues are deal-breakers or if they can be addressed through negotiations with the seller.

11. What time of the year is best to buy a home?

It depends on whether your goal is to find the best deals or a broad spectrum of options. A 2016 analysis indicates that November is the best time to locate a decent deal, while April is the most active month for new listings. August appears to be a good middle month, with affordable pricing and a large number of available properties.

12. What is an Earnest Money Deposit?

A buyer makes a deposit to a seller as an indication of their good faith or assurance of interest in purchasing the house. Earnest money is not always refundable. However, as long as buyers do not breach any agreements and follow decision deadlines, they often receive their earnest money back.

13. How much Down Payment do I need to pay to buy a house?

Ideally, you can avoid paying private mortgage insurance (PMI) by making a 20% down payment; however, in practice, lenders typically want a minimum of 3% in order for the sale to proceed. Certain lenders could demand a minimum of 5%, depending on your location and the type of mortgage you qualify for.

Real Estate FAQs Related to Financing Options For Home Buyers

1. What is a Mortgage?

Before buying a home, most people need a mortgage, where they borrow money from a lender using the property as collateral. The mortgage agreement details terms like loan amount, interest rate, and repayment period.

2. What are the pros and cons of Conventional loans for real estate FAQs?

Conventional loans have both advantages and disadvantages. One of the main benefits is that if you have a high credit score and a substantial down payment, you may be eligible for a lower interest rate. Additionally, conventional loans do not require mortgage insurance if you make a down payment of at least 20%. However, these loans usually require a higher credit score compared to government-backed loans, and the down payment requirements can range from 3% to 20% of the purchase price. It’s essential to weigh these factors and consider your financial situation before deciding on a conventional loan.

3. How do FHA loans work, and who qualifies for them?

FHA loans are a popular choice for first-time homebuyers and those with lower credit scores. These loans are insured by the Federal Housing Administration and are more accessible to borrowers who may not qualify for conventional loans. FHA loans typically require a down payment of 3.5% of the purchase price and have more lenient credit score requirements. However, keep in mind that FHA loans require mortgage insurance premiums, which can increase your monthly payments. To qualify for an FHA loan, you must meet certain criteria, including having a steady income and a debt-to-income ratio within acceptable limits.

4. What are the benefits of VA loans for military personnel?

VA loans offer several advantages for veterans and active-duty military personnel. One of the main benefits is that VA loans often do not require a down payment, making homeownership more accessible. Additionally, VA loans do not require private mortgage insurance, which can save borrowers a significant amount of money each month. These loans also have more lenient credit requirements compared to conventional loans. It’s important to note that VA loans are only available to eligible veterans and military personnel and may have limitations based on service history and length of service.

5. What is Earnest Money?

Earnest money, often referred to as a good faith deposit, is a sum of money provided by a buyer to demonstrate their serious intent to purchase a property. It is usually 1-2% of the home’s price, held in escrow.

How To Navigate The Negotiation Process an Real Estate FAQs

1. Why is it important to respond promptly to offers?

When selling a home, responding promptly to offers is crucial for several reasons. First, it shows potential buyers that you are serious about selling and willing to engage in negotiations. Prompt responses demonstrate professionalism and can help build trust between you and the buyer. Additionally, delaying your response may give the impression that you are not motivated to sell or that you have received better offers. In a competitive market, delaying your response can result in missed opportunities and potential buyers moving on to other properties.

2. What should I consider when Reviewing Offers?

When reviewing offers, it’s essential to consider more than just the purchase price. Evaluate the terms and contingencies outlined in each offer. Look for offers with favorable financing terms, such as a substantial down payment or a pre-approval letter from a reputable lender. Consider the proposed timeline for inspections, appraisals, and closing. Assess any contingencies, such as the sale of the buyer’s current home or the need for repairs. Your real estate agent will help you review and compare offers, weighing the pros and cons of each to determine the best course of action.

3. How can a Counteroffer benefit me as a seller?

A counteroffer allows you, as the seller, to propose alternative terms to the buyer’s initial offer. It gives you an opportunity to negotiate and potentially secure more favorable terms or a higher purchase price. Counteroffers can be used to address concerns or contingencies outlined in the buyer’s offer. It’s important to work closely with your real estate agent to determine the appropriate counteroffer strategy. They will help you navigate the negotiation process, advise on potential repairs or credits, and ensure that your interests are protected throughout the transaction.

The Importance Of Working With a Real Estate Professional

1. Why should I work with a Real Estate Professional when buying or selling a home?

Working with a real estate professional provides numerous benefits when buying or selling a home. Professionals have extensive knowledge of the local market and can provide valuable insights into pricing, neighborhoods, and market trends. They have access to a wide range of resources and can help you find suitable properties or attract potential buyers. Professionals are skilled negotiators and will advocate for your best interests throughout the transaction. Whether you’re buying or selling, a real estate Professional will guide you through the process, handle paperwork, and ensure a smooth and successful transaction.

2. How do I choose the right Real Estate Professional an another Real Estate FAQs?

Choosing the right real estate professional is crucial for a successful home buying or selling experience. Start by asking for recommendations from friends, family, or colleagues who have recently worked with.

Conclusion

Real estate transactions are often complex, and it’s essential to have a clear understanding of the process to make informed decisions. That’s why we’ve compiled this real estate FAQs list. We have address common concerns and provide expert answers that will guide you through your real estate journey. Whether you’re a first-time buyer or an experienced seller, these frequently asked questions will give you the information you need to navigate the market successfully.

You may feel more equipped to handle the real estate market for real estate FAQs now that you have the answers to some of the most often-asked questions about selling and buying real estate. If you have any other queries related to buying and selling your home or want to consult real estate experts for real estate FAQs, you can directly get in touch with us here.

Real estate investing is usually seen as a profitable choice for those looking to diversify their investment holdings. You have a lot of options when looking for real estate investment opportunities. Yet, single-family houses have always been a popular option among investors.

At first, investing in multi-family homes could appear like an excellent decision because of the high potential ROI. But when you take into account the upkeep costs of a multi-family home in addition to several other considerations, you might want to reconsider the kind of property you are willing to invest in.

Multi-family properties can help you to scale up your investments at a rapid pace. However, single-family houses can be a smart real-estate investment for some good reasons such as higher stability, simpler and easier financing, more control, and diversification opportunities.

Also, compared to multi-family properties, single-family homes, sell quickly, and appreciate more swiftly.

So, let’s try to dig deeper and understand better why single-family houses are a smart real estate investment.

Here, we go!

What Is A Single-Family House?

Simply put, a single-family house is a separate home with no walls or floor in common with any other residence.

In a single-family home, the building and the land it is situated on are owned by the same person. In contrast, the owner of a condo shares joint ownership of shared facilities with other association members and only has a legal claim to the interior of their unit.

Additionally, single-family homes are not entitled to share any utilities, HVAC systems, or air conditioning units with other residences. They have direct access to the street and their own separate entrances and exits.

Why Should You Invest In A Single-Family House?

- Multiple Financing Options

Compared to financing a multifamily property, financing a single-family home is easier to do and more practical. Moreover, you can usually receive lower down payments.Conventional mortgages, private loans, and real estate partnerships are some of the options for financing the purchase of a single-family home for investment. By using a conventional home loan product, you can be pretty confident that a 20 percent down payment will help get the deal done.However, you can also utilize many of the same commercial loans that multi-family property investors use to finance a single-family home.To ascertain which course of action is best for your particular circumstances, speak with lenders or financial experts. - Greater Control

You have more control over your investments when you make single-family house purchases.You can sell a single-family house at any moment if you decide later on that investing isn’t the correct move for you. You are in greater control of the investment and the duration of your investment.They also offer less stress when investing because they appreciate quickly over time and require less maintenance from the investor’s perspective. - Stable Rental Income

Most single-family rentals have long-term tenants with fewer turnovers than multifamily rentals. This is because tenants usually like the privacy and space that a single-family home offers, which makes it simpler for investors to locate long-term tenants and sustain a steady income. Not only this but investors experience less stress because long-term tenants are more reliable and will pay their rent on time. - More Choices Available

There are plenty of single-family houses to select from, as they account for about 70% of the housing market. With just a little digging, you can score some amazing deals. Purchasing a property with equity from the start is crucial, and it shouldn’t be just any old house from the multiple listing service. Your wealth and portfolio will grow consistently and safely with the help of this value. - Low Risk Involved

Investing in single-family homes is an excellent method to begin real estate investment without taking on excessive risk. Single-family home sales are always increasing, so even if your investment doesn’t work out as expected, you can still sell it later and recoup the majority of your costs. - Easier Selling

You can sell your portfolio of single-family homes separately or as a group. You can advertise them to retail customers or business investors. If you’d like, you can sell some and keep the others.Capitalization rates and debt coverage ratios do not restrict retail buyers. Often, they will pay the appraised value, which is not tied to local rental incomes. A single-family home can usually be sold in a few months, but selling an apartment block or multi-family property could take years. - Potential Capital Gains

Single-family homes generally show an appreciation trend over time; when the housing market improves, the value of these properties rises, offering potential capital gains to investors. - Facilitates Easy Property Management

Because single-family homes are smaller than multi-unit buildings, they are less complicated and more affordable to maintain. Tasks related to property management, like upkeep, repairs, and leasing agreements, get easier to handle. - More Privacy

If you prefer privacy, a single-family house is the type of property just for you. With no shared walls or floors, single-family homes give you more privacy and space than other types of residential buildings. - Exit Flexibility

When it comes to exit plans, single-family homes provide various options. Depending on the condition of the market and your financial objectives, as an investor you can decide whether to sell the property, rent it out for a long time, or even turn it into a vacation rental.

The Final Say

Investors seeking to increase their wealth through real estate may find that investing in single-family houses is a fulfilling endeavor. It’s a desirable option because of the consistent rental income, potential for appreciation, and easy property management.

Nevertheless, investors must also take into account single-family home’s higher acquisition prices, constrained scalability, and volatile market.

Performing comprehensive research, assessing personal financial goals, and seeking advice from real estate experts. It can all assist in reducing risks and optimizing returns in this area of investing.

Need expert consultation? Get in touch with Elite Properties today!

Buying a home is an exciting experience in and of itself. It becomes even more thrilling when you see the variety of options that are available for you to invest in. The single-family home and the town house are two of the most preferred options. However, how can one decide which one to choose?

It can be tough to compare town houses and single-family homes and decide which option is best for the home you want to buy. However, this ultimately relies on a lot of factors, including your spending limit, your need for privacy and space, your propensity for house maintenance, and so on.

So, let us help you to understand more and dive deep so that you can make the right decision.

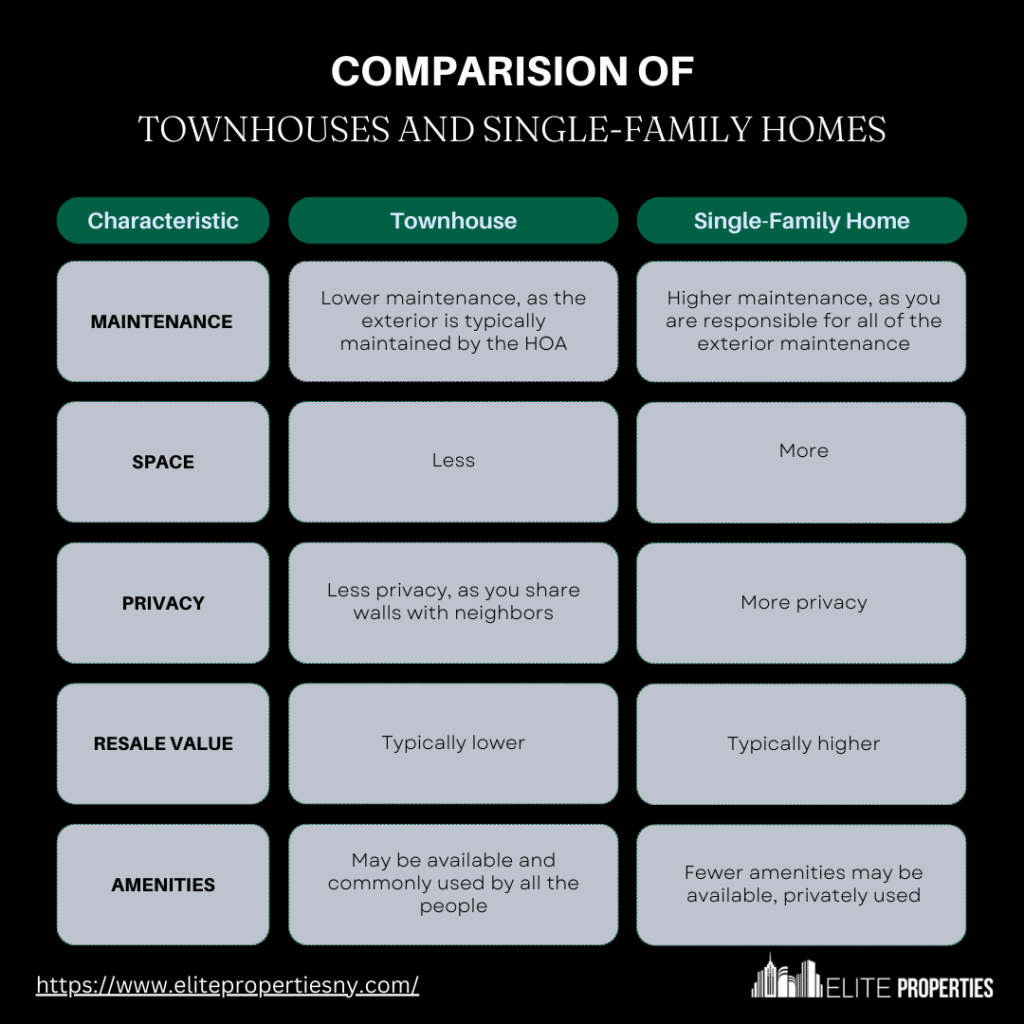

Defining Town Houses vs. Single-Family Homes

Townhouses and single-family homes each have their pros and cons, so determining which is right for your family comes down to your needs and priorities.

- Space and Privacy

Townhouses typically offer less space and privacy since they share walls with neighbors. However, single-family homes usually provide more square footage and yard space, as well as greater seclusion. It quiet and privacy are important, a detached single-family home may suit you best. - Affordability and Amenities

Townhouses are generally more affordable and often include amenities like a gym, pool, playground that would cost extra with a single-family home. The trade-off is less control over changes to the property and potentially higher homeowners association (HOA) focs If budget and community facilities matter most a townhouse could he ideal. - Maintenance and Responsibility

With a townhouse, the HOA usually handles exterior maintenance like landscaping, roofing, and siding repairs. Single-family homeowners are responsible for all maintenance costs and duties. If less maintenance responsibility is a priority, a townhouse may require less effort. - Resale Value

Historically, single-family homes appreciate more over time and sell faster than townhouses. However, townhouse values can also rise substantially, especially if located in a desirable neighborhood. Much depends on the housing market, so for the best resale potential, consider both location and style of home.

In the end, analyze what really counts for your family’s lifestyle. A townhouse or single-family home- either can be the perfect choice when you make the decision that suits your needs.

Town House Pros

It affordability and shared amenities top your list, townhouses are worth serious consideration. Townhouses offer lower costs than single-family homes, in large part because the land and structure are shared among multiple units. Your HOA fees cover maintenance of shared spaces like entryways, parking lots, and recreation areas.

- Lower Costs

Townhouses are often significantly less expensive than comparable single-family homes. You’re only paying for your unit and a share of the common areas, rather than an entire structure and lot. HOA foes, which typically cover insurance, landscaping, repairs, and amenities, are usually lower than what you’d pay to maintain a whole house and yard yourself. - Shared Amenities

Most townhouse communities offer recreational facilities like swimming pools, playgrounds, gyms or clubhouses that you share with your neighbors. Not having to budget for and maintain these amenities yourself is a huge benefit for many homebuyers. Your kids can enjoy splash pads, sports courts and play structures right in your neighborhood.

Townhouse living does mean less privacy and more noise from shared walls. But for many homebuyers, especially first-timers, the compromises are well worth the savings. It affordability and an active community are priorities for your family, townhouses deserve strong consideration. With lower costs of living and built-in amenities, they offer an appealing combination of value, convenience and lifestyle.

Single-Family Home Pros

- A single-family home offers some appealing benefits over a townhouse. If privacy and personal space are high priorities, a detached house may be the way to go for your family.

- With no shared walls, you’ll enjoy peace and quiet without hearing your neighbors. You can play music, watch TV, or do home improvements without worrying about bothering others or being bothered in return.

- A single-family home also provides more usable outdoor space that you don’ have to share. You’ll have your own private yard for kids and pets to play gardening entertaining, or just relaxing.

- Inside, a single-family house typically offers more square footage and storage space. There are no constraints on layout or design, so you can customize the floor plan to suit your needs. A detached home, gives you the freedom and flexibility to configure the space as you like.

- While a single-family home may cost more upfront and in ongoing expenses like utilities, the privacy spaciousness, and customization can be well worth the investment for many homebuyers. For growing families or those who simply want more room to spread out, a detached house is appealing. If resale value is a concern, single-family homes also tend to hold their value very well over time compared to townhouses.

- In the end, you need to weigh all these factors and determine what will work best for your family’s lifestyle and budget. But when it comes to privacy, space, and freedom of design, a single-family home is hard to beat.

Town House Cons

- One of the biggest downsides to townhouses compared to single-family homes is less privacy and limited personal outdoor space. Since townhouses share walls with neighboring units, you lose a degree of privacy.

- You may be able to hear your neighbors at times through the walls, and they can likely hear you as well. This can be frustrating if you have a family that is prone to making a lot of noise.

- For families with children or those who enjoy outdoor entertaining and recreation, the limited space can feel cramped.

- There’s little room for activities like barbecuing, gardening, playing sports or riding recreational vehicles.

- You’re also at the mercy of any homeowners association (HOA) rules regarding what is and isn’t allowed in the communal outdoor areas.

Single-Family Home Cons

As a homeowner, the costs and required maintenance for a single-family home are typically higher than for a townhouse. Before you fall in love with the idea of a big yard and no shared walls, make sure you understand the financial responsibilities that come with it.

- Higher Property Taxes

Single-family homes usually have higher property tax rates since the land and structure are privately owned. The average property tax payment for a single-family home in the US is over $3,500 per year. Property taxes are used to fund schools, infrastructure, and public services in your area. The more valuable and spacious the property, the higher the tax bill. - Increased Utility Bills

It costs more to heat, cool, and power a larger space. Utility bills for a single-family home can easily exceed $200-$500 per month depending on the season and region. The open floor plan and additional rooms also mean more area to furnish and decorate, adding to your costs. - Pricier Maintenance and Repairs

Expect to pay higher prices for maintenance like lawn mowing, hedge trimming, gutter cleaning, and snow removal since there’s more ground to cover. Any repairs or replacements to the home’s structure, roof, siding, windows, plumbing or electrical systems will also cost significantly more. Homeowners spend an average of $2,467 on maintenance and home emergency costs yearly. For a single-family home, that number is likely higher. - Limited Time for DIY

Doing maintenance and repairs yourself can save money but requires free time and skills. As a homeowner, your time is often limited by work and family responsibilities Hiring contractors and service professionals is convenient but adds to your overall housing costs significantly over the lifetime of the home.

While a single-family home offers privacy and freedom, weigh the responsibilities carefully. The financial obligations require proper budgeting and the time requirements may limit your flexibility. For some, a townhouse is a more practical and affordable choice. But with realistic expectations about costs, a single-family home can be very rewarding.

Town House vs. Single-Family Home: Major Differences

- Concept And Structure

The structure is the most apparent difference here. Townhouse are build in close to each other. In such a way they shares at least one wall with another next to them. On the other hand, single-family homes are freestanding and do not share common areas or common walls with any other property. They are usually situated on a property that is owned by the homeowner. However, the piece of land on which a townhome is built is also owned by its owner. This land often comprises little front and backyard spaces too. - Location

Townhomes gained their term since they are generally found in urban regions close to larger cities. In comparison, a single-family home can be found anywhere, even in remote, rural, and sparsely populated areas. But this could only be interesting and fun unless you enjoy a vivid nightlife. - Maintenance And Care

You are responsible for all upkeep and maintenance when you own a single-family home. This means that in order to maintain your home in good shape, you’ll need to mow the lawn, replace the smoke detector and air filter batteries, clear the gutters, and perform all other necessary maintenance. In townhouses, you’re typically a member of a larger community association, which will take care of many of those bigger chores for you, especially the outside ones. They may also manage other common maintenance aspects of the community, such as the garden and yard, the roof, and the gutters. - Size

Townhouses can be constructed as separate buildings arranged side by side on a single property, or as a row of attached buildings. Generally, a town house consists of two units, each having its own staircase and door. Normally, the apartments are assembled with shared walls. On the other hand, a single-family home is a large residence with a common living area for all the family members, including parents and kids, who live under one roof. - Affordability

The price is yet another important distinction between townhouses and single-family homes. Because townhouses are smaller and use less space than single-family homes, they usually have better affordability. A single-family home, on the other hand, provides greater space and amenities. These are typically found in well-kept neighborhoods where residents may enjoy privacy while being close to their loved ones. Therefore, they cost slightly more than a townhouse. - Amenities

More amenities could be available in a townhouse than in a single-family home. These may consist of an on-site maintenance staff, a fitness center, and a common pool. It is in a prime location near restaurants, retail establishments, and public transit. Although it can be very costly, most families would rather drive a few miles to enjoy their privacy by living in a single-family home close to the town center with all the conveniences.

Which Is The Better Investment?

There is no single answer to whether you should invest in a townhouse or a single-family home. Choosing between these two options largely depends on your financial situation, various choices, and requirements. Each has the potential to be a good investment option. However, here’s what you can consider.

- Townhouses are usually a good option if you’re a first-time buyer who wants to be close to the city center and other facilities.

- A single-family home is suitable for people. As they appreciate privacy more and have more outside space.

- The cost of a single-family home is usually higher than that of a townhouse. It does, however, provide greater autonomy and liberty. Additionally, since there will be enough room for guests and vehicles. Also hosting larger events at your single-family home can be simpler than at someone else’s.

- Single-family homes are typically enormous and provide a lot more room for family members to live peacefully. It offers additional privacy, which increases appreciation and resale value.

- Townhouses are more affordable if your only goal is to make an investment; their price per square yard is higher. Over time, you can build equity without incurring the greater costs associated with buying a single-family home. But if you require access to liquid assets or anticipate moving in less than five years, a townhouse may not be a wise purchase.

- Single-family homes, on the other hand, would cost more but are simpler to sell. This is because freedom and privacy are fundamental human desires and are important considerations when purchasing a home.

- You might not be able to recover your initial investment quickly as townhomes are comparatively more challenging to sell than single-family homes.

- In the end, let’s not forget that the location and the kind of customers you serve have an impact on the resale as well. Considering this, you can decide to invest in a single-family home. If the majority of your target customers are affluent and wealthy enough to purchase single-family homes in elite to decent areas.

- If your intended customers do not have enough credit limit. Nevertheless, you ought to choose a townhouse that is somewhat less expensive.

Lifestyle Factors to Consider for Your Family

When choosing between town houses and single-family homes consider how each option would suit your family’s lifestyle and needs. Some key factors to consider includes:

- Privacy and Space

Single-family homes typically offer more privacy and space. You’ll have your own yard, basement, attic, and garage. Town houses usually feature analer private outdoor space, if any, and less storage, However, the close-knit community feel of town houses may appeal to some families. Think about how much space and alone time each family member values. - Amenities and Activities

Town houses often come with amenities like pools, playgrounds, and recreation centers that can benefit health and community Families with young children or active lifestyles may prefer these built-in amenities. Single-family homes usually require paying for gym memberships or other activities separately. Consider now much your budget allows for discretionary spending on amenities and entertainment. - Maintenance and Upkeep

Single-family homes generally require more upkeep like yardwork, repairs, and general maintenance. Town houses typically handle outdoor maintenance, landscaping, and some utilities, reducing the amount of work for homeowners Busy familles may appreciate less responsibility for home maintenance. However, single-family homes do provide more control over your living space, Determine how hands-on you want to be with home repairs and yardwork. - Affordability

Town houses are usually more affordable especially if you have a limited budget. Homeowners association fees cover certain costs Single-family homes typically cost more but may build equity faster. Think about your current financial situation and future financial goals to choose the option that fits your budget.

Considering these lifestyle factors and your family porkies can help determine whether a town house or single family home the best choice for your needs. Make a list of must-haves for your living situation to guide your decision making. And down forget you can always reevaluate down the road!

Financing and Budgeting for Each Options

When considering financing options for a townhouse or single-family home, budgeting and planning are key. Think through all the costs involved to determine what you can truly afford before you start house hunting.

- Down Payment

The down payment for a townhouse or house is typically 3-20% of the purchase price. The higher your down payment, the lower your interest rate and monthly payment will be. For a $300,000 home, a 20% down payment would be $60,000, if that’s not feasible, aim for at least 5% down to qualify for a mortgage. - Mortgage Options

Mortgages for townhouses and houses are basically the same. The two most common types are fixed-rate and adjustable-rate mortgages (ARMS). A fixed-rate mortgage has the same interest rate for the life of the loan, typically 1530 yoard Ar ARM usually has a lower initial rate that adjusts up or down depending on the marker ARMS often start with 3/1 or 5/1 terms, faing the rate for 3-5 years before adjustments. - Property Taxes and Insurance

Property taxes and homeowners insurance are annual housing costs to budget for Property taxes are based on the assessed value of the home and vary significantly by location Insurance protects your investment and typically costs $500-$2,000 per year Get estimates for both to determine your annual escrow payment which is often included in your monthly mortgage bill. - HOA Fees (for Townhouses)

If purchasing a townhouse, factor in homeowner’s association or HOA fees, which typically cover building insurance, exterior maintenance, amenities, and utilities. HOA fees average $200-$500 per month but can be higher for luxury townhouses Make sure you understand what’s included before purchasing. - Ongoing Costs

Aside from your mortgage payment, property taxes, insurance, and any HOA fees, budget for ongoing maintenance costs like heating/cooling, electrical, plumbing, yard care, and general repairs which average $200-$500 per month for a single-family home. Townhouses have lower maintenance costs since the HOA covers exterior upkeep.

With proper planning and budgeting, you can find a home that meets your needs without becoming house poor, Determine what you can afford, compare all costs, and make the choice that allows you to live comfortably while building equity.

Town House vs. Single-Family Home FAQS

As you weigh town houses versus single-family homes, you likely have some questions. Here are a few common FAQs to help clarify the differences.

1. Are townhouses more affordable than single-family homes?

Typically, yes. Townhouses are often more budget-friendly since the cost of the land and structure is shared among multiple owners. Monthly fees also usually cover exterior maintenance, insurance, and amenities. However, townhouse association fees can be pricey. Single-family homes usually have lower or no association fees but higher upfront costs to purchase the property and home.

2. Do I have more privacy in a single-family home?

Absolutely. Single-family homes offer far more privacy since you don’t share any walls with neighbors. You have your own yard and entryway. Townhouses provide less privacy since you share walls, and often a yard and entryway, with adjacent homes. If peace and quiet are a priority, a single- family house is probably your best choice.

3. Is there more responsibility with a single-family home?

Yes, owning a single-family detached home typically means more responsibility. You are solely responsible for all maintenance, repairs, property taxes, insurance, and utilities. With a townhouse, the association handles many exterior responsibilities like landscaping, roofing, siding, and insurance. You’re still responsible for interior maintenance and utilities.

4. Can I rent out or resell either type of property?

Both townhouses and single-family homes can potentially generate income through renting, reselling, or both. However, single-family homes usually have higher resale values and appeal to a wider range of buyers. Townhouses may be easier to rent or sell to families or those seeking low- maintenance living. Check with your homeowners association for any restrictions or renting before you buy.

5. What are the amenities like for each?

Amenities can vary significantly between properties. However, townhouses often offer access to community amenities like a pool, gym, playground or recreation center. Single-family homes typically do not come with shared amenities, so you would need to pay for any additions yourself. Of course, some single-family home neighborhoods do offer communal amenities that homeowners can access for a fee.

Conclusion

So there you have it, a look at the key differences between town houses and single-family homes to consider for your family. While a single-family home offers more privacy and space, a town house provides lower costs and less maintenance. Evaluate your priorities and lifestyle needs. Do frequent neighborhood interactions and shared amenities appeal to you? Or would you prefer more independence and control over your own property? Whatever you decide, make sure to think it through carefully. After all, this is one of the biggest decisions you’ll make for your family’s shelter and comfort. But with the right choice for your unique situation, you’ll find a place to call home for years to come.

Hope this helps you in making the right decision whether to invest in a town house or a single-family home. If you are looking for more professional guidance to ace your investment get in touch with Elite Properties. Learn more.

If you are hoping to maximize profits on your home sale, placing a “For Sale By Owner” sign in the front of your house is an appealing option as real estate brokers take away a good amount of commission from the sale proceeds.

But as a seller, are you ready to take up all the responsibilities that a listing agent would normally take? Well, that’s what a “For Sale By Owner” method of selling demands.

You are required to undertake the work yourself to save money and maintain control if you don’t hire an agent to handle it for you. Well, this isn’t always simple.

So is ‘For Sale By Owner’ the right choice for you?

Let’s find it out!

What is ‘For Sale By Owner’?

In simple words, a property that is listed as ‘For Sale By Owner’ (FSBO) can be purchased directly from the owner rather than through a real estate agent or broker. The acronym FSBO is commonly pronounced as ‘fizz-bow’.

Some sellers prefer to go this route to avoid paying agent commissions, which typically range from 5% to 6% of the sale price and are split between the seller’s listing agent and the buyer’s agent, if any.

However, FSBO sales, while less expensive for the owner, also have their own set of costs. In an FSBO transaction, the seller has to undertake all the responsibilities of a listing agent.

So, let’s have a look at some of these responsibilities further.

What Are The Responsibilities Of The Seller In FSBO?

Below are some of the responsibilities that an FSBO seller has to undertake:

- Doing market analysis to establish the worth of your home.

- Choosing a fair sales price.

- Listing your house, creating the description, and adding images.

- Making and printing promotional items.

- Advertising your home.

- Coordinating individual showings and open homes.

- Taking care of all the inquiries from potential customers.

- Addressing all inquiries from the buyer’s agent.

- Negotiating with interested people.

- Qualifying prospective consumers.

- Dealing with legal paperwork.

How Much Does FSBO Cost?

While selling a house yourself is less expensive, there are some costs you’ll still incur. These may consist of:

- Fees for professional cleaning.

- Professional photography fee.

- Fees for virtual staging.

- Fees for MLS listings.

- Repair expenses.

- Attorney fees.

- Other legal costs if any.

- Home appraisal fee.

- Buyer’s agent commission, if any.

Pros Of ‘For Sale By Owner’

Here are some reasons why you should consider FSBO.

- 1. Save On The Commission

The primary drive for FSBO is to avoid paying the listing agent commission. Typically, sellers pay 5-6% of the sales price of the home as the agent’s commission from the sales proceeds. This could help you save on the commission fees. For instance, if your house is sold for $250,000 and the commission charged by the agent is 5% of the sales price, you’ll have to pay the agent $12,500 from the sale proceeds.Nonetheless, please note that you still have to pay the buyer’s agent commission if any. - 2. Take Control

The absence of a middleman in your dealings with purchasers and/or their agents will give you full control over how things will work.It implies that you’ll have the final say about your home’s listing price, the upgrades you make, the people you show it to, and eventually, the buyer.You can decide which proposals to take into account and how to advertise your house. Selling FSBO can be the best option for you if you prefer the notion of keeping control. - 3. Better Sales Pitch

Nobody knows your house like you do. You have personal experience with what it’s like to live in your neighborhood and be a part of the community. Your sales pitch could become strong if you share all that you love about your home with the prospective buyer. All of those details can be included in the advertising copy and other selling efforts to promote the sale of your home.

Cons Of ‘For Sale By Owner’

Below are some of the drawbacks of FSBO. Have a look!

- 1. Can’t Escape The Buyer’s Agent Commission

When you pay a commission to your listing agent, the agent working on behalf of the buyer may also receive about half of the commission that you pay to your agent. This means the 2-3% buyer’s agent commission will still be due if you decide to sell your home yourself. Therefore, in the case of the $250,000 property sale, you would only have saved money if you sold it yourself and paid the buyer’s agent a 2.5% commission which amounts to $6,250. - 2. Lot Of Work

When selling your home under FSBO, you’ll have to do a lot of work including everything that a real estate agent would do.You’ll have to prepare your home for sale, analyze comps to price it correctly, handle marketing activities, set up appointments and showings, provide offers, and negotiate. There is also a tonne of paperwork required to do. - 3. Lack Of Real Estate Knowledge

For inexperienced sellers in particular, legal terms, acronyms, and other sorts of jargon can be extremely daunting. You can only rely on your knowledge and the resources you have available if you are selling your house on your own.There are many free resources available, but since every transaction is unique, choosing the best course of action can be challenging.

Final Thoughts

A FSBO offers the chance to avoid paying commissions of thousands of dollars. But it takes time, and it’s not for everyone.

However, spending time and money on your listing, consulting an appraiser and attorney, and getting the greatest price possible will help guarantee a smooth transaction.

However, it is better to hire a local real estate agent if you attempt selling FSBO and decide it’s not for you, or if you simply think selling your house yourself would be too much work.

For more profound guidance, you can get in touch with us!

When a house has been abandoned for a long time, it is generally because of financial or legal issues.

Selling an abandoned house can be a challenging thing to do, especially if you’re not familiar with the process. You’ll need to make repairs to the house if you list it in the classifieds or work with a real estate agent to attract more potential buyers. Nonetheless, nobody wants to invest additional money in a house they don’t care much about. A lot of people want to sell the house as-is and profit financially from doing so.

But the longer the property remains abandoned, the more it falls into disrepair, which can further complicate matters when it comes to selling it.

But don’t worry; in this blog, we will guide you through how can you prepare yourself for selling your abandoned house.

So, let’s jump in!

Understanding The Concept Of Abandoned Properties

The concept of abandoned property refers to houses that have been left vacant or neglected for various reasons. These abandoned houses can present a lucrative opportunity for real estate investors, as they often come at a lower price and can be renovated or repurposed for profit.

However, dealing with abandoned properties comes with its own set of challenges. Squatters can pose legal issues, as their presence complicates the ownership and sale process. Additionally, adverse possession laws can impact the ownership rights of abandoned properties, potentially leading to disputes.

Yet comprehending the intricacies of abandoned properties, investors and buyers can navigate this market effectively.

Why Do Owners Abandon Houses?

Financial difficulties, such as unpaid wages or high property taxes, can drive homeowners to abandon their houses. Crime rates in the area may also play a role in house abandonment.

Foreclosure and the inability to afford necessary repairs or maintenance are some other factors that can lead owners to abandon their properties.

Additionally, some owners may not have contact information for potential buyers or realtors leading to the house to stay abandoned.

The Impact Of Neglect On Abandoned Houses

Neglected abandoned houses can attract squatters and pose safety risks, making them a potential hotspot for criminal activities. Moreover, the lack of regular upkeep and maintenance can lead to significant structural damage, causing the property value to plummet.

Besides, these neglected houses often become breeding grounds for pests, which not only affects the immediate vicinity but also contributes to neighborhood blight.

Additionally, fire hazards, like damaged wiring or non-functional fireplaces, can be present in abandoned houses, further escalating the safety concerns associated with these properties.

To mitigate these issues, it’s crucial to address the neglect and restore these homes before putting them on the market.

Selling An Abandoned House: Primary Challenges And Solutions

Finding buyers for abandoned properties can be difficult due to their poor condition. One solution is to consider cash offers, which can help sell the property quickly. Another option is to work with experienced realtors who specialize in dealing with abandoned houses.

However, potential buyers may be hesitant to purchase these properties because of the potential need for extensive repairs. To overcome this challenge, it is crucial to provide accurate and detailed information about the property’s history and condition.

By addressing these significant challenges, sellers can increase their chances of finding buyers for abandoned houses.

How To Sell An Abandoned House Without Investing More Money Into It?

Selling an abandoned house without additional investment is possible through virtual staging, online marketing, and emphasizing the property’s potential.

Besides, flexible financing options and highlighting the investment opportunity can attract buyers willing to renovate.

Importance of Location in Selling Abandoned Properties

When selling abandoned properties, the location plays a crucial role in determining their market value and demand. Factors such as access to transportation, schools, and shopping centers can greatly increase the appeal of the property. It is important to research local real estate trends and demand to understand the potential buyer pool.

Additionally, understanding the neighborhood’s reputation and crime rates is essential when marketing abandoned properties, as it affects the level of safety and desirability for prospective buyers.

Providing contact information for local authorities or community organizations can also offer reassurance to potential buyers. By considering these aspects, sellers can effectively highlight the importance of location and attract interested parties to purchase the abandoned properties.

Virtual Staging For Selling An Abandoned House

Virtual staging can play a crucial role in selling an abandoned house. It allows potential buyers to visualize the property’s potential and see it in a whole new light.

By adding virtual furniture, decor, and landscaping, the space can be transformed into an appealing and inviting atmosphere.

Virtual staging also offers the flexibility to showcase different design styles, catering to a wider range of buyer preferences and increasing the chances of attracting interested buyers. Moreover, high-quality virtual images can grab attention and generate increased interest in the property.

The best part is that virtual staging is a cost-effective and time-saving alternative to traditional home staging methods, making it a valuable tool for selling abandoned houses.

Potential Buyers For Abandoned Properties

Potential buyers for abandoned properties usually include:

- Real estate investors seeking profitable opportunities.

- First-time homebuyers willing to invest in renovations.

- House flippers specializing in renovating and reselling properties.

- Local developers or builders looking for land for new construction projects.

- Non-profit organizations focused on revitalizing neighborhoods.

Bottom Line

Selling an abandoned house can be a tough process, but with the right strategies and approach, it can be done successfully.

Attracting buyers for abandoned properties with land requires highlighting the importance of location and showcasing the potential of the property. Virtual staging can also play a significant role in visualizing the possibilities of an abandoned house. Additionally, renovations can greatly increase the value of abandoned houses and attract potential buyers.

It’s important to identify the target market for abandoned properties and tailor your marketing efforts accordingly. By implementing these strategies, you can successfully sell your abandoned house and maximize its value.

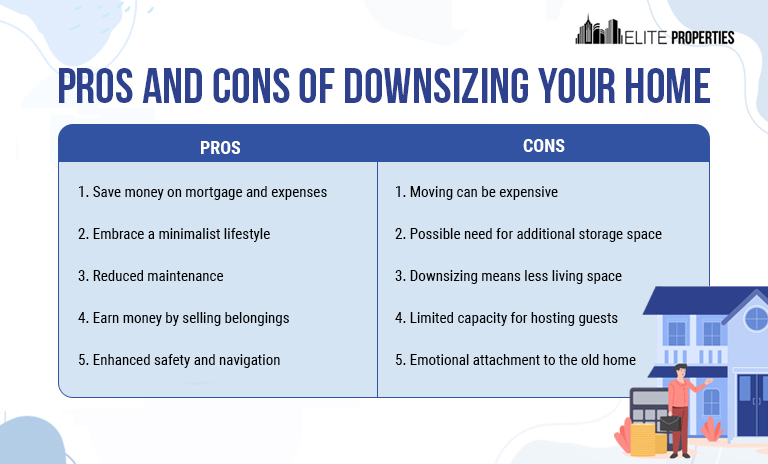

As you are near retirement, it’s a good time to start thinking about downsizing your home. The idea of moving into a smaller space can be daunting, but the benefits are huge.

Downsizing can have a significant impact on savings and financial planning for retirement. By selling a larger home, you can free up funds that can be used to boost your retirement savings. It can also mean less maintenance and fewer responsibilities for you to worry about in retirement.

In this guide, let’s try to take a closer look at downsizing so that you can enjoy a stress-free transition into your new home for retirement.

We’ll also provide tips on how to start the process of decluttering and organizing your current home, as well as how to sell your house and move to a smaller property. So, let’s dive in!

Understanding The Concept Of ‘Downsizing’

Moving to a smaller home for retirement is what downsizing entails. It offers the advantages of reduced maintenance and lower expenses due to the smaller space.

People often consider downsizing when they retire, as it can be a strategic financial decision, allowing individuals to save money and allocate resources efficiently.

By embracing a smaller home, you can optimize their living situation and create a more manageable space. This transition offers the opportunity to let go of unnecessary belongings and focus on a simpler and more fulfilling lifestyle.

Benefits of downsizing your home

Downsizing refers to the process of moving from a larger home to a smaller one, typically to simplify and streamline your lifestyle. The benefits of downsizing can be numerous.

- It can free up a significant amount of money by reducing mortgage payments, property taxes, and utility bills.

- Downsizing can lead to a more manageable and easier-to-maintain living space, allowing for more time and freedom to pursue other activities.

- Downsizing can encourage a more minimalist lifestyle, helping to declutter and simplify your belongings.

However, downsizing is not without its challenges. Letting go of sentimental items and adjusting to a smaller living space can be emotionally and mentally taxing. Furthermore, it requires careful planning and consideration to ensure that the new home meets your needs and accommodates your lifestyle.

Challenges of downsizing your home

- Financial freedom and reduced expenses

One of the most significant benefits of downsizing your home is the potential for financial freedom. By moving to a smaller property, you can significantly reduce your mortgage payments, property taxes, and utility bills. This can free up a substantial amount of money that can be used for other purposes, such as saving for retirement, traveling, or pursuing hobbies and interests. Additionally, downsizing can help you eliminate unnecessary expenses associated with maintaining a larger home, such as higher insurance costs and expensive repairs.

- Simplified and easier-to-maintain living space